Sending money to another country can feel a bit daunting, but the traditional bank international money transfer is a process that's been trusted for decades. You can think of it as a highly secure postal service for your money, using a global network to move funds from your bank account to someone else's, wherever they might be.

How Bank International Money Transfers Work

When you set up an international transfer, you’re not actually sending a bundle of cash across the border. What really happens is your bank sends a series of secure electronic messages to the recipient's bank. These messages are instructions to release an equivalent amount of local currency to the person you're paying. It’s all built on a foundation of trust and long-standing agreements between banks worldwide.

This whole system hinges on a central communication network that connects almost every financial institution on the planet. The main player keeping everything in sync is the Society for Worldwide Interbank Financial Telecommunication, which everyone just calls SWIFT.

The Role of the SWIFT Network

Picture SWIFT as the grand, central post office for the entire global banking system. It doesn’t physically touch the money. Instead, it handles the payment orders—the "letters"—that tell banks exactly where to send funds. Almost every international wire transfer you make will travel along this messaging network to make sure the instructions are safe, standardised, and end up at the right place.

Understanding these messaging systems is key to grasping how money truly moves around the world. To get a better handle on this, learning about the role of SWIFT in international transfers provides a much deeper insight.

Correspondent Banks The Connecting Flights

Here’s where it gets a little more complex. Your bank in South Africa probably doesn't have a direct line to a small local bank in rural Canada. This is where correspondent banks, sometimes called intermediary banks, step in. They act like the "connecting flights" for your money transfer.

Think about it like this: a transfer from a bank in Johannesburg to a small town in Canada might first get routed through a huge banking hub like London or New York. That major bank then forwards it to the final destination. Each stop along this chain can add extra time and, you guessed it, extra fees.

This multi-step journey is precisely why a bank transfer is incredibly reliable but not always the fastest or most cost-effective way to send money. The more banks involved in the chain, the longer it can take and the more hidden fees can pop up along the way.

To wrap your head around the key features of a standard bank transfer, this table breaks it down.

International Bank Transfers at a Glance

| Feature | Typical Characteristic | What This Means for You |

|---|---|---|

| Network Used | SWIFT Network | Highly secure and globally recognised, but can be slow. |

| Speed | 2-5 business days | Not ideal for urgent payments as delays are common. |

| Cost Structure | Sender fees + Intermediary fees + Poor exchange rates | The final amount the recipient gets can be unpredictable. |

| Tracking | Often limited or non-existent | It can be hard to know exactly where your money is. |

| Reach | Virtually any bank account, anywhere | Unmatched global coverage, reaching almost every corner of the world. |

Ultimately, while the bank transfer system is built for security and reach, its complexity often leads to higher costs and slower delivery times compared to more modern alternatives.

The Journey Your Money Takes Across Borders

Ever wondered what actually happens after you click ‘send’ on a bank international money transfer? It’s easy to imagine your money zipping across the globe instantly, but the reality is a lot more complex. Think of it less like an email and more like a passenger taking a series of connecting flights to reach a distant city.

Your funds don’t travel a direct route. Instead, they’re passed from your bank to one or more intermediary banks before finally being cleared for deposit into your recipient's account. Each one of these ‘layovers’ adds time and, often, cost to the process.

The SWIFT Network in Action

The entire journey is orchestrated by the SWIFT network, which basically acts as the air traffic control for global finance. When you start a transfer, your bank sends a secure SWIFT message—a highly detailed set of instructions—out into this network. This message hops from bank to bank, authorising each one to process the transaction and pass it along the chain.

Let's say you're sending money from Johannesburg to a small town in Germany. Your transfer might first stop at a large correspondent bank in London. From there, the London bank relays the instructions to a major German bank in Frankfurt, which finally directs the funds to the correct little branch. This intricate, multi-step process is precisely why a seemingly simple digital transaction can take anywhere from two to five business days to complete.

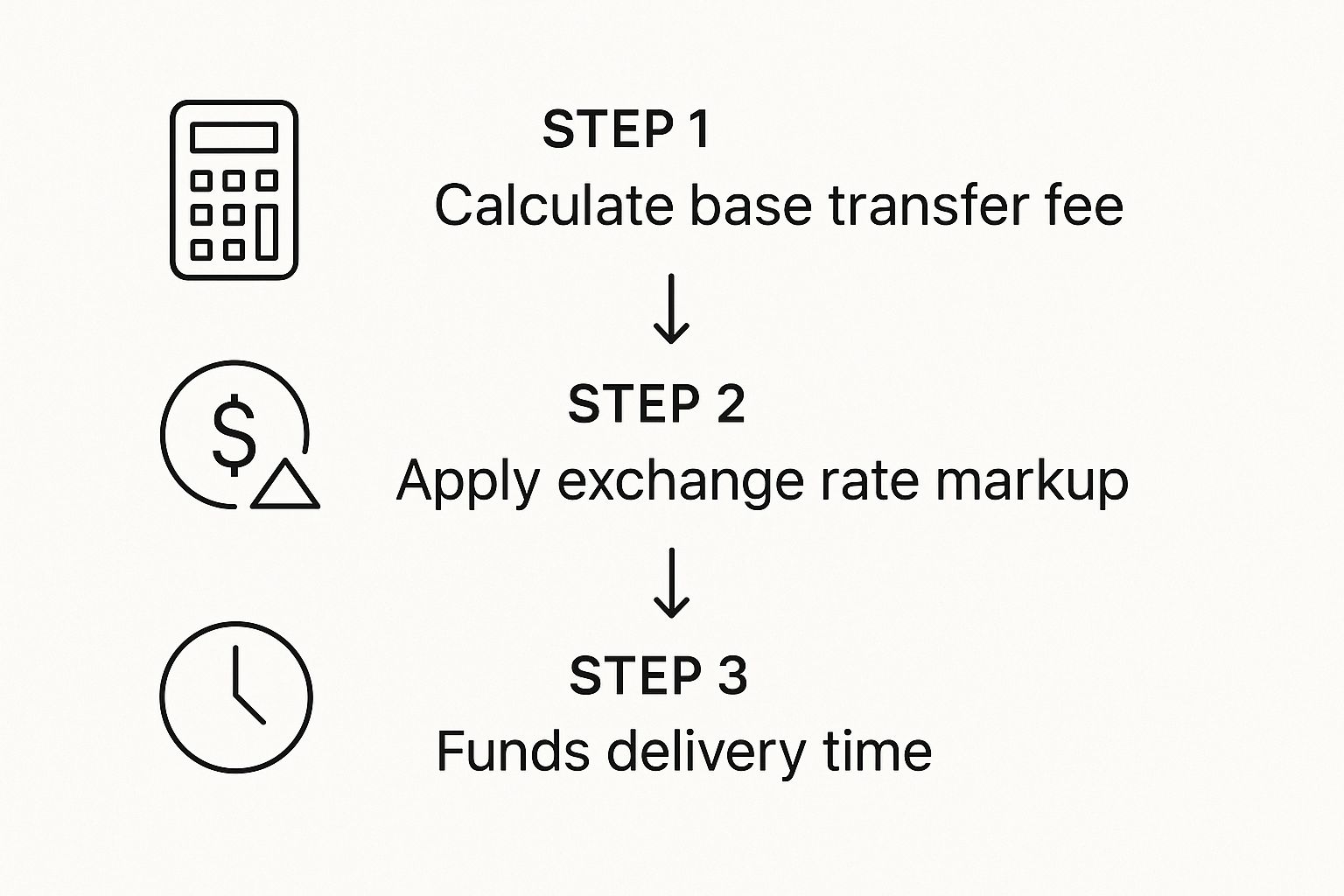

This infographic breaks down the key stages that influence the total cost and delivery time of your transfer.

As you can see, various factors like fees and exchange rates are applied at different points before your funds finally arrive.

Navigating with SWIFT Codes and IBANs

To make sure your money doesn't get lost on this complicated journey, two critical pieces of information are needed. You can think of them as a highly specific address and postal code for your funds.

SWIFT/BIC Code: This is an 8 or 11-character code that identifies a specific bank anywhere in the world. It’s like the unique airport code for the destination bank (e.g., JNB for Johannesburg), ensuring your money is routed to the correct financial institution.

IBAN (International Bank Account Number): The IBAN pinpoints the specific individual account at that bank. If the SWIFT code gets the money to the right airport, the IBAN is like the passenger's exact seat number, making sure the funds land with the right person.

Key Takeaway: An incorrect SWIFT code or IBAN is the number one reason for transfer delays or outright rejections. The single most important thing you can do for a smooth transaction is to double-check these details before you confirm the payment.

This long-established network is incredibly reliable for moving money safely. However, its dependence on multiple intermediaries is exactly why it can be slow and why you sometimes see unexpected fees deducted along the way—a topic we'll get into next.

Decoding the True Cost of Your Transfer

When your bank advertises a fee for a bank international money transfer, what you’re seeing is rarely the final price. Think of it as the tip of the iceberg. The most significant costs are often lurking just beneath the surface, and understanding them is the only way to know what you’re really paying to send money abroad.

There are two main charges to look out for. The first is the one everyone sees: the upfront, fixed transfer fee. The second, which is usually the real killer, is the exchange rate markup.

The Hidden Cost in the Exchange Rate

Here’s a secret banks don’t shout about: you almost never get the real exchange rate. That rate you see on Google or on the news? That’s the mid-market rate, and banks apply a markup, or a ‘spread’, on top of it.

In simple terms, they sell you foreign currency for a little more than it's worth and buy it back for a little less. It's a built-in commission that's not clearly itemised on your statement. A seemingly tiny difference of 2-4% on the rate can add a huge amount to the cost of a large transaction, often making that initial transfer fee look like pocket change.

Example in Action:

Imagine the mid-market rate is R18.50 to $1, and you need to send $5,000 to a supplier. At the real rate, this would cost you R92,500.But your bank offers you a rate of R19.00 to $1. At this marked-up rate, the same $5,000 now sets you back R95,000. That R2,500 difference is the hidden fee, paid entirely through the poor exchange rate.

The Mystery of Correspondent Bank Fees

Ever sent a specific amount, only for the person on the other end to receive less than you intended? The culprit is usually a correspondent or intermediary bank fee.

As your money travels through the SWIFT network, each bank that handles it along the way can take a slice for processing. These fees are completely unpredictable because your bank often has no control over which other banks get involved or what they decide to charge. This makes it impossible to know the final cost upfront.

This isn’t just a minor inconvenience; it’s a recognised global issue. In sub-Saharan Africa, the average cost to send just $200 is a staggering 8.4 percent, making it the most expensive region in the world for remittances. International bodies and our own South African Reserve Bank are actively working on reforms to tackle these high fees. You can read more about the efforts to improve cross-border payments in our region on resbank.co.za.

Once you add up the initial transfer fee, the exchange rate markup, and any surprise correspondent bank charges, the total cost of a bank international money transfer can be far higher than you ever expected. Knowing this empowers you to ask the right questions and start comparing your options more intelligently.

What to Expect: Transfer Times and Regulations

Ever wondered why sending money across the world can feel like it's travelling by horse and carriage? It's a fair question. When you make a bank international money transfer, several factors come into play that can stretch the timeline, and it’s almost never instant. The journey your money takes is shaped by everything from global time zones to public holidays.

Think about it: a transfer you kick off on a Friday afternoon in South Africa might not even get looked at by a bank in the US until their Monday morning. If you throw in a public holiday on either side, a transfer that should take three days can easily drag on for a week. The number of correspondent banks involved also makes a big difference; each "stop" on the route adds more processing time.

Getting to Grips with South African Compliance

Beyond the practical delays, there's a whole layer of regulations to navigate, especially here in South Africa. Every single cross-border payment is subject to the exchange control regulations laid out by the South African Reserve Bank (SARB). These rules are there to keep a close eye on the capital flowing in and out of the country.

What this means for you is that you can’t just send money without a good reason. Your bank is legally obligated to ask for the "why" and report it.

For South African businesses, this isn't just a bit of admin—it's non-negotiable. If you don't provide the right documents, your transfer can be blocked or held up for ages, which can cause serious headaches for your supply chain or international payroll.

The Paperwork You'll Need

To make sure your transfer sails through without a hitch, you’ll need to have your documents in order. The specifics can differ slightly from bank to bank, but you should always be prepared with the following:

- Proof of Identity (FICA): Your bank has to have your up-to-date FICA documents on file. It’s a standard check to prevent money laundering.

- Reason for Payment: You’ll have to state exactly what the money is for, whether it's paying an overseas supplier, an employee's salary, or covering import costs.

- Supporting Invoices or Agreements: For any business payment, you'll almost certainly need to provide a copy of the invoice or contract that backs up the transfer. This is to prove it's a legitimate transaction.

Understanding these rules is vital. In South Africa, these transfers are the lifeblood of regional and international trade, making the country a key hub for payments. The problem is, the costs can be a real barrier. The average cost of sending money from South Africa can be anywhere from 5% to 8%, which is well above the target set by the UN. You can find more details about remittance costs in Africa on remitscope.org.

By getting a handle on both the potential delays and the compliance hurdles beforehand, you can get your paperwork sorted and time your payments better, saving yourself from a lot of frustrating and expensive hold-ups.

Comparing Banks with Modern Fintech Alternatives

For a very long time, if you needed to send money overseas, your local bank was pretty much the only option. An international money transfer through a bank was the standard, the default, the only game in town. But the financial world has changed dramatically. A new wave of technology-driven companies, known as fintechs, has completely shaken things up, offering services that are often faster, cheaper, and a whole lot clearer.

The old-school banking system relies on something called the SWIFT network. Think of it as a series of connecting flights for your money. It's incredibly secure, but each "layover" at a different bank along the way can add time and, you guessed it, extra fees.

In contrast, many fintechs have built their own payment networks from the ground up. This is more like a direct courier service. By cutting out all those expensive middlemen, your money gets where it's going without the costly detours. This is the fundamental difference that explains the huge gap in speed and cost you see today. While a bank might still be the go-to for really complex, high-value corporate deals, fintechs are now a far better fit for most day-to-day business payments.

Key Differences in Cost and Speed

Put a traditional bank transfer side-by-side with a fintech service, and the differences are glaring. Banks tend to bundle their charges in a few different ways: there's the upfront fee you see, the poor exchange rate they give you, and often, hidden fees from intermediary banks that you only discover later. In fact, research shows that for every 1% increase in the cost of sending money, the actual amount sent drops by 1.6%. Those high fees really do eat into your bottom line.

Fintech providers approach this completely differently. They usually offer the real mid-market exchange rate—the one you see on the news—and charge a single, small, transparent fee. That clarity is a game-changer. You know exactly what it will cost before you even press "send".

The real power of fintech lies in its transparency. You're not left guessing about surprise fees, and you avoid the significant loss that comes from a bad exchange rate. This means your recipient gets the full amount you intended, every time.

Making the Right Choice for Your Business

So, when should you use a bank and when should you opt for a fintech? It really comes down to what you need to do. A bank provides a level of institutional security that might be non-negotiable for massive, multi-million rand deals that involve things like letters of credit or complex trade finance. For a deeper dive into these foundational institutions, you can get more information by understanding the banking and credit union industry.

However, for the vast majority of regular business tasks—paying overseas suppliers, settling invoices with international freelancers, or managing payroll for remote teams—fintech services offer undeniable advantages in both efficiency and cost savings.

Let's break down the head-to-head comparison to make it crystal clear.

Bank Transfers vs Fintech Solutions: A Head-to-Head Comparison

This table offers a straightforward look at how the old way of sending money stacks up against the new.

| Feature | Traditional Bank Transfer | Modern Fintech Service |

|---|---|---|

| Speed | 2-5 business days, with potential delays. | Often same-day or even instant. |

| Exchange Rate | A marked-up rate with a hidden 2-4% spread. | The real mid-market rate with no markup. |

| Fees | Multiple fees (sending, receiving, intermediary). | A single, low, transparent fee. |

| Transparency | Very low; the final received amount is often a surprise. | High; you see the exact cost and received amount upfront. |

| User Experience | Often requires branch visits and paperwork. | Entirely digital, with easy online platforms. |

As you can see, the choice often comes down to weighing the institutional familiarity of a bank against the clear performance benefits of a modern fintech platform. For most businesses today, the efficiency gains are simply too significant to ignore.

Common Questions About Sending Money with a Bank

Sending money overseas with a bank can feel like a bit of a maze. It's a process with a lot of moving parts, regulations, and potential hiccups that can be pretty confusing. To help clear things up, we’ve put together answers to the questions we hear most often from people sending money across borders.

Getting your head around these practical points can save you a lot of headaches and make the whole experience a lot smoother.

Is It Safer to Use a Bank for International Transfers?

This is a big one. The short answer is that both traditional banks and modern, regulated fintech services are very secure. Banks have been around forever, they're built like fortresses, and they operate under incredibly strict rules. This makes them feel like the gold standard for safety, especially if you're moving a massive sum or handling a complex corporate deal.

But let's be clear: licensed fintech companies aren't playing around with security either. They're also regulated by financial authorities and use top-tier encryption to protect your money. So, what’s "safest"? It really comes down to your situation. For a multi-million rand transaction where institutional backing is paramount, a bank is a solid bet. For your day-to-day business payments, a reputable fintech service is just as secure—and a whole lot more efficient.

Can My International Bank Transfer Actually Get Lost?

It’s almost unheard of for money to just vanish into thin air within the SWIFT system. Every single transfer is tagged with unique reference numbers, so it's tracked every step of the way. What happens far more often, though, is that transfers get stuck, delayed for ages, or bounced back completely.

The usual culprit? A simple mistake in the details. A typo in an account number, a wrong IBAN, or an incorrect SWIFT/BIC code can bring the whole thing to a grinding halt.

When a transfer gets rejected, the money does eventually make its way back to your bank. The problem is, this reverse trip can take weeks, and you’ll often be charged extra admin fees for the trouble. That means you get back less than you sent. The takeaway? Double-check, then triple-check every single detail before you press that button.

What Information Will I Need in South Africa?

To get a transfer out of South Africa, you'll need a specific set of details for the person you're paying and to satisfy our local compliance rules.

- Recipient’s Full Name and Address: Make sure it's an exact match to what's on their bank account.

- Their Bank Account Number or IBAN: The IBAN is the standard format for Europe and many other parts of the world.

- Their Bank’s Name and Full Address: It's often wise to get the specific branch details too.

- The Bank’s SWIFT/BIC Code: Think of this as the bank's international postal code.

On the South African side, your bank will also ask for:

- Your FICA Documents: Your proof of identity and address need to be current.

- The Reason for the Transfer: You have to declare why you're sending the money (e.g., "Payment for imported goods").

- Supporting Paperwork: If it's a business payment, you'll almost certainly need to provide an invoice or contract.

Why Did the Recipient Get Less Money Than I Sent?

Ah, the most common frustration of all. You send a specific amount, but less arrives on the other side. The reason is almost always hidden fees from intermediary or correspondent banks.

As your money zips across the SWIFT network, it often hops between several banks before reaching its final destination. Each of these "helper" banks can take a slice for their trouble, deducting a processing fee directly from your money. Your own bank often has no idea what these charges will be, which makes it impossible for them to tell you exactly how much will land. This is a huge difference compared to good fintech services, which can often guarantee the final received amount down to the last cent.

Ready to bypass the high fees and uncertainty of traditional bank transfers? Zaro offers South African businesses access to real exchange rates with zero hidden markups. See how much you can save on your next international payment by visiting https://www.usezaro.com.