Choosing the right bank account is one of the most critical financial decisions for any South African business, from solo entrepreneurs to growing SMEs. Hidden fees, complex pricing structures, and outdated services can silently drain your profits and create unnecessary administrative burdens, especially for companies dealing with international trade or managing lean operations. This guide cuts through the marketing noise to deliver a practical analysis.

We have meticulously reviewed the market to find the cheapest business bank account options that do not compromise on essential features. This comprehensive resource list is designed to help you make an informed decision quickly and confidently. We will explore everything from zero-monthly-fee digital accounts ideal for startups and BPO businesses to powerful fintech solutions created to slash international transaction costs for exporters. Each entry includes a breakdown of its fee structure, core features, honest limitations, and screenshots, giving you a clear view of its real-world value.

This isn't just a list; it's a strategic tool. Get ready to compare, contrast, and select the perfect financial partner to support your business's growth. We provide the direct links you need to get started, saving you time and, most importantly, money.

1. Zaro

Best For: Businesses managing cross-border payments.

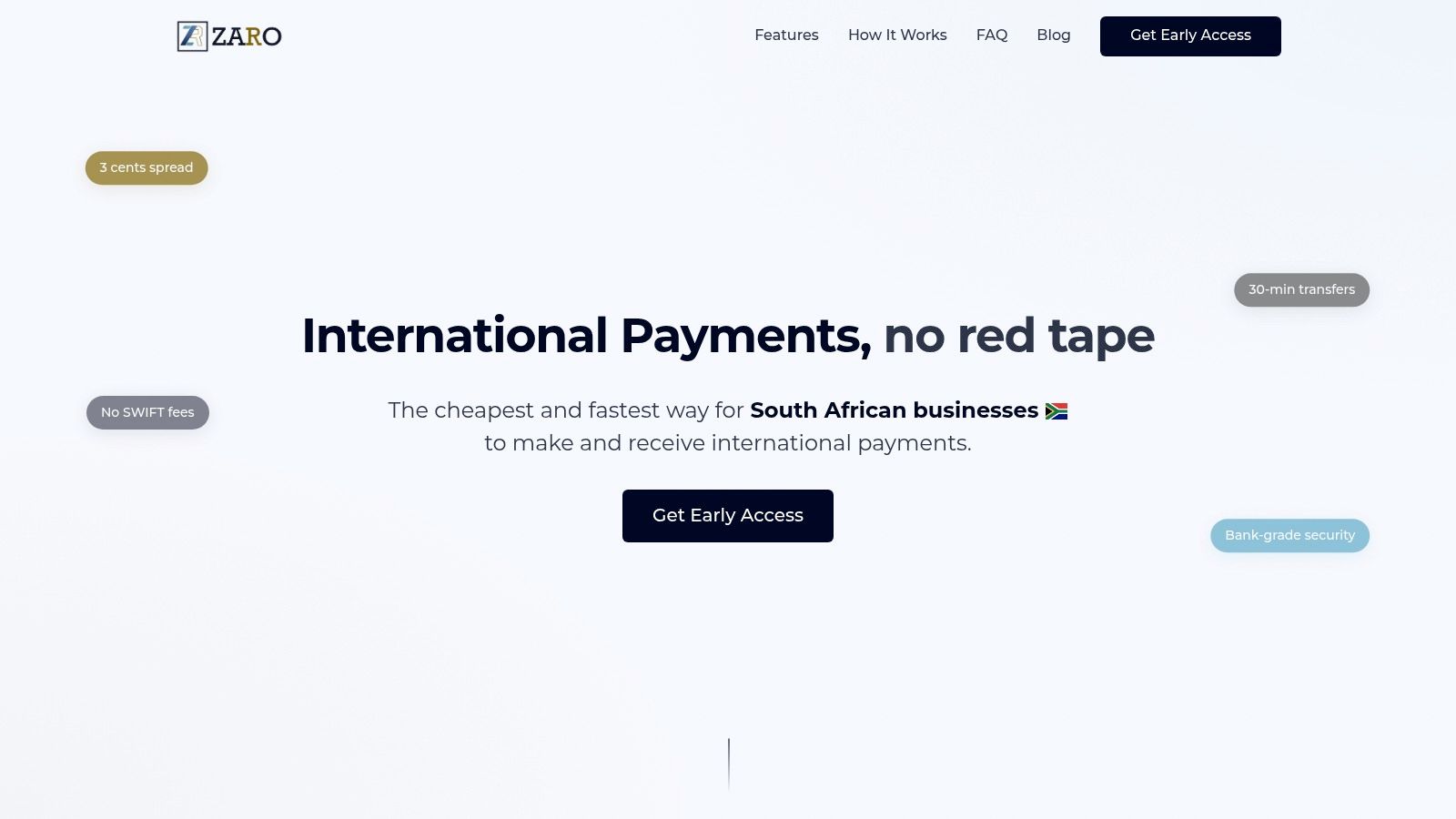

Zaro stands out as a premier choice for South African businesses that frequently transact internationally, offering a powerful alternative to traditional banking that dramatically cuts costs. While not a conventional bank account, its specialised focus on foreign exchange (FX) and international payments provides a compelling solution for importers, exporters, and BPO businesses seeking one of the cheapest ways to manage multi-currency finances. Zaro redefines value by eliminating punitive SWIFT fees and hidden costs, positioning itself as an indispensable tool for optimising international cash flow.

The platform's core strength lies in its transparent and ultra-competitive FX rates. Businesses can exchange currency at a razor-thin spread of just 3 cents (approximately 0.17%) above the real-time interbank rate. This exceptional rate structure directly translates to significant savings on every transaction, making it a frontrunner for the title of the cheapest business bank account for global operations. For a company managing large-volume transfers, these savings can profoundly impact the bottom line.

Key Features and Practical Use Cases

Zaro’s feature set is meticulously designed for financial control and efficiency. The platform supports both ZAR and USD accounts, which can be easily funded via standard bank transfers. A standout feature is its enterprise-grade security, offering multi-user access with customisable permissions. This allows a CFO to grant specific transaction approval rights to a finance manager while providing view-only access to an accountant, ensuring robust governance and operational security.

Real-World Application: An export business receiving USD payments can use Zaro to accept funds in under 30 minutes, convert them to ZAR at a near-perfect rate, and avoid the typical 3-5 day settlement delays and high fees charged by traditional banks. The included ZAR and USD debit cards further empower businesses to spend globally, directly accessing these favourable rates for online subscriptions or supplier payments without incurring hefty conversion markups.

Pros and Cons

Pros:

- Extremely Low FX Spread: The 0.17% markup is significantly lower than bank-offered rates, maximising your returns on currency conversion.

- Rapid International Transfers: Payments from the US can settle in as little as 30 minutes, a massive improvement over standard SWIFT timelines.

- No Hidden Fees: Zaro eliminates SWIFT charges and other surprise costs, ensuring complete transparency.

- Robust Security: Multi-user access and custom permissions provide excellent financial governance for teams.

- Convenient Debit Cards: Spend directly from your ZAR and USD balances with dedicated debit cards.

Cons:

- Niche Focus: Currently tailored specifically for South African businesses engaged in international trade.

- Expanding Ecosystem: As a fintech, its range of integrations may not yet match that of long-established banking institutions.

Website: https://www.usezaro.com

2. FNB First Business Zero Account

Best For: Sole Proprietors and Startups with Low Transaction Volumes

FNB's First Business Zero Account is a powerful contender for the title of cheapest business bank account, specifically tailored for sole proprietors. It eliminates the monthly account fee, a significant barrier for new entrepreneurs managing tight cash flow. This account is designed for businesses with an annual turnover of up to R5 million, making it a perfect starting point for freelancers, consultants, and small home-based enterprises.

What makes it stand out is the combination of zero cost with access to FNB's robust digital ecosystem. While many entry-level accounts skimp on features, this one provides unlimited free card swipes and comprehensive tools via the FNB App and Online Banking. The inclusion of free access to Fundaba, FNB’s business coaching platform, offers genuine value beyond basic banking, helping new owners learn essential business skills.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R0 |

| Eligibility | Sole Proprietors (annual turnover < R5m) |

| Card Swipes | Unlimited, free |

| Key Benefit | Access to business coaching (Fundaba) |

| Withdrawals/Deposits | Charged per transaction |

Our Assessment

The primary limitation is its strict eligibility, as it's only available to sole proprietors. This means partnerships, private companies (Pty) Ltd, and other business structures need to look elsewhere. The account's cost-effectiveness also diminishes if your business handles a lot of cash, as deposit and withdrawal fees apply. However, for a digital-first sole trader who primarily receives electronic payments and pays suppliers via card, this account is practically free to operate.

Website: FNB First Business Zero Account

3. Absa Business Evolve Lite

Best For: New Businesses Wanting a Pay-As-You-Use Model from a Major Bank

Absa's Business Evolve Lite account enters the competition for the cheapest business bank account with a straightforward, no-frills approach. It features a zero monthly fee, making it highly attractive for startups and small enterprises with an annual turnover of up to R1.5 million. This account operates on a purely pay-as-you-use basis, ensuring you only pay for the transactions you actually perform.

What sets it apart is the combination of a zero-fee structure with the backing of a major financial institution. This provides access to Absa's extensive branch network and a dedicated business service desk, which is a significant advantage for businesses that might need in-person support. While basic, the inclusion of free online banking, a Visa Debit Card, and free NotifyMe services covers all the essential digital needs for a modern, cost-conscious business.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R0 |

| Eligibility | Annual turnover < R1.5m |

| Online Banking | Included, free |

| Key Benefit | Access to Absa's support network |

| Transactions | Pay-as-you-use model |

Our Assessment

The primary appeal of the Evolve Lite account is its simplicity and predictability. If your transaction volume is low or irregular, the pay-as-you-use model can be exceptionally cost-effective. However, its main limitation is that costs can escalate quickly for businesses with high transaction volumes, particularly those involving cash deposits or frequent EFT payments. For a new business that needs the reliability of a big bank without committing to a fixed monthly fee, this account provides a perfect, low-risk entry point into business banking.

Website: Absa Business Evolve Lite

4. Nedbank Startup Bundle

Best For: New Businesses Needing Initial Support and Mentorship

Nedbank’s Startup Bundle is designed to ease the financial burden during the critical first few months of operation. It provides a six-month holiday on monthly fees for new sole proprietors and private companies (with an annual turnover under R3 million), making it an excellent choice for entrepreneurs who need to preserve capital while establishing their business. This bundle is more than just a bank account; it's a launchpad for growth.

What sets this offering apart is the combination of a temporary fee waiver with valuable business-building resources. The inclusion of 20 free digital transactions per month encourages a move to efficient, modern banking practices from day one. Access to SimplyBiz, a platform offering business registration services, templates, and networking opportunities, provides tangible support beyond pure banking, making this one of the most supportive options for a new venture.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R0 for the first 6 months |

| Eligibility | Sole Proprietors & Pty Ltds (< R3m turnover) |

| Digital Transactions | 20 free transactions per month |

| Key Benefit | Access to SimplyBiz business tools |

| Post-Offer Period | Pay-as-you-use fees apply after 6 months |

Our Assessment

The primary appeal of the Nedbank Startup Bundle is its introductory six-month, zero-fee period. This provides significant breathing room for a fledgling business to find its feet. However, businesses must plan for the transition to a pay-as-you-use model once the promotional period ends, as costs can increase depending on transaction volume. The real value lies in the bundled support tools, which can be instrumental for a founder navigating the complexities of starting a company. This makes it an ideal, if temporary, cheapest business bank account for ambitious startups.

Website: Nedbank Startup Bundle

5. Standard Bank MyMoBiz Account

Best For: New Businesses Needing Simple Digital Banking and Payment Tools

Standard Bank's MyMoBiz Account offers an accessible and affordable entry point for entrepreneurs. With a minimal monthly fee, it positions itself as a strong contender for the cheapest business bank account for those just starting out. This account is designed for simplicity, providing essential digital banking features without the complexity or higher costs of more advanced packages. It is an ideal fit for new ventures that need professional banking credentials and the ability to accept digital payments from day one.

What truly sets MyMoBiz apart is its integration with PocketBiz, a mobile point-of-sale solution. This allows businesses to accept card payments on the go using a smartphone, making it incredibly practical for mobile service providers, market vendors, and pop-up shops. The combination of a low-cost account with an integrated payment acceptance tool provides significant value and empowers small businesses to trade professionally.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R7 |

| Eligibility | Startups and small businesses |

| Key Benefit | Access to PocketBiz for card payments |

| Free Transactions | Limited (pay-as-you-transact) |

| Digital Access | Full access to Standard Bank’s digital platforms |

Our Assessment

The MyMoBiz account is an excellent choice for businesses prioritising a low fixed monthly cost and digital functionality. Its biggest advantage is providing a gateway to accepting card payments through PocketBiz, a feature often associated with more expensive accounts. The main limitation is the pay-as-you-transact model for most transactions beyond the monthly fee, which can become costly for businesses with high transaction volumes. However, for a new business that operates primarily online and needs a straightforward, low-maintenance account with payment capabilities, the R7 monthly fee is hard to beat.

Website: Standard Bank MyMoBiz Account

6. Capitec Business Account

Best For: Small Businesses Seeking Simplicity and Transparent Fees

Capitec brings its renowned simplicity and transparent pricing from personal banking to the business world. The Capitec Business Account is a strong contender for any small to medium-sized enterprise that values a straightforward, no-frills approach. Its single, low monthly fee structure eliminates the guesswork often associated with complex banking costs, making it a predictable and affordable option.

What makes this account particularly appealing is its seamless integration for existing Capitec clients. Business owners can manage both their personal and business finances within a single, user-friendly app, simplifying financial oversight. The focus on a core transactional offering ensures that essential banking functions are efficient and cost-effective, without the distraction of features a smaller business might not need. This makes it an excellent choice for businesses prioritising clarity and control over their banking expenses.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R65 |

| Eligibility | All business types (Sole Proprietor, Pty, etc.) |

| Inter-Account Transfers | Free (between your own Capitec accounts) |

| Key Benefit | Integrated personal and business banking on one app |

| Digital Banking | Robust and user-friendly mobile and online banking |

Our Assessment

The Capitec Business Account’s strength lies in its simplicity and transparent fee model, making it a reliable and cheap business bank account. The ability to manage everything from one app is a significant convenience. The primary drawback could be its more limited physical branch network compared to legacy banks, which might be a concern for businesses that frequently handle large cash deposits or require in-person services. However, for a digitally savvy business that values ease of use and predictable costs over a large branch footprint, Capitec offers a compelling and modern banking solution.

Website: Capitec Business Account

7. TymeBank EveryDay Business Account

Best For: Digital-First Sole Traders and Freelancers

TymeBank’s EveryDay Business Account cements its position as one of the cheapest business bank account options by leveraging a digital-only model to eliminate monthly fees. This account is designed for modern entrepreneurs, freelancers, and sole traders who are comfortable managing their finances entirely online or through an app, without the need for traditional branch-based services. It offers a streamlined, fast, and accessible banking solution.

What sets this account apart is its sheer simplicity and speed. The registration process is remarkably quick, often completed in minutes online. Unlike many competitors, TymeBank offers the added benefit of earning interest on positive account balances, allowing your working capital to generate a small return. This makes it a compelling choice for businesses that maintain a cash buffer and prefer a fully digital experience from a disruptive player in the banking sector.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R0 |

| Eligibility | Sole Proprietors (must be registered on TymeBank app) |

| Card Swipes | R0 |

| Key Benefit | Earn interest on positive balances, rapid online setup |

| Withdrawals/Deposits | Charged per transaction (at Pick n Pay/Boxer till points) |

Our Assessment

The primary drawback of the TymeBank Business Account is its complete reliance on a digital infrastructure and its partner retail network (Pick n Pay and Boxer) for cash services. Businesses that require frequent, complex, in-branch consultations or handle large volumes of cash might find this model restrictive. However, for a service-based sole proprietor who receives payments electronically and values a low-cost, no-fuss banking solution, TymeBank is exceptionally cost-effective. The account is practically free for users who avoid cash transactions, making it an ideal choice for the modern digital entrepreneur.

Website: TymeBank EveryDay Business Account

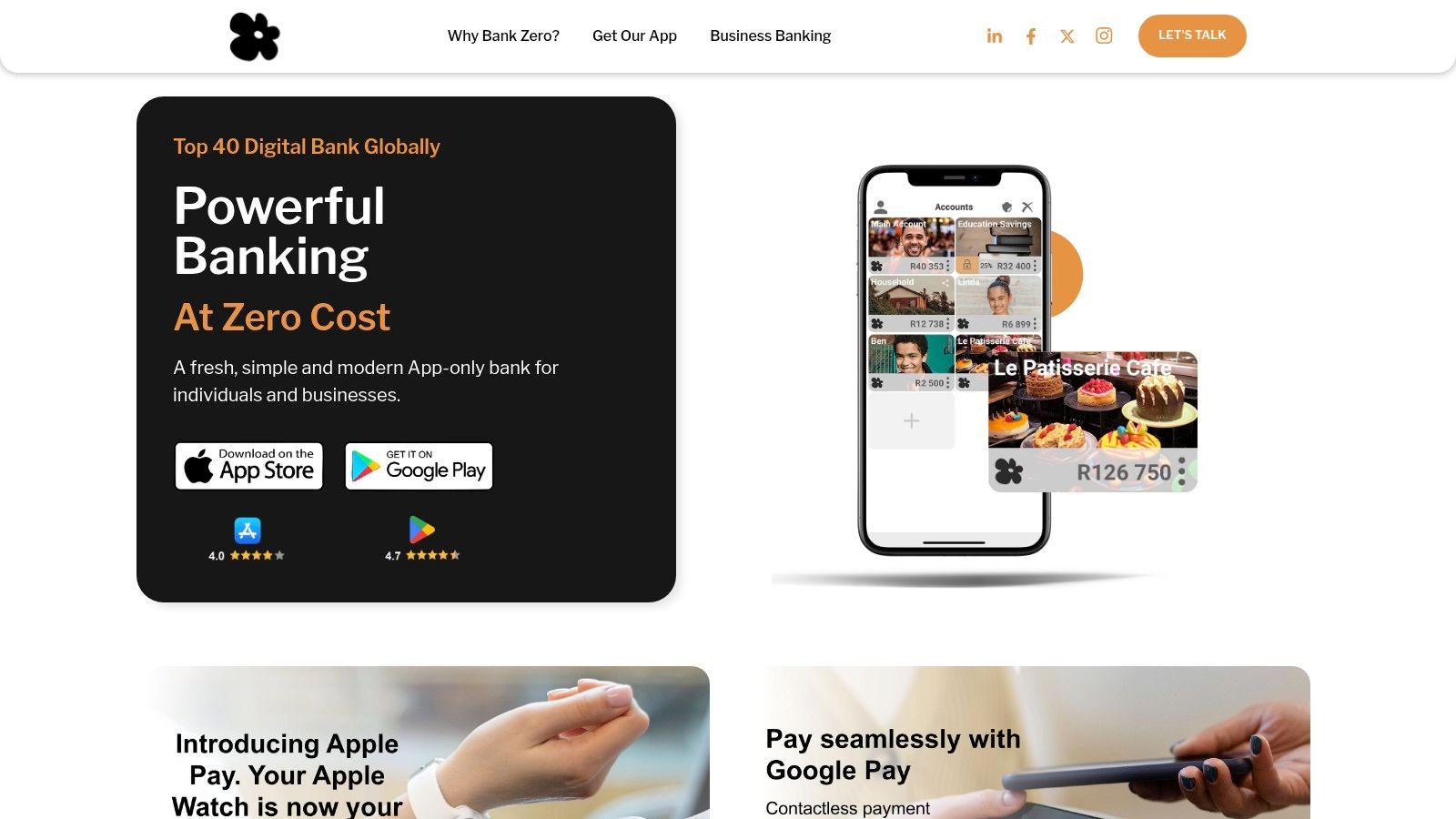

8. Bank Zero Business Account

Best For: Tech-Savvy Businesses and Teams Requiring Granular Control

Bank Zero emerges as a formidable digital-only contender, offering what is arguably the cheapest business bank account for companies that operate entirely online. Co-founded by tech entrepreneurs, its platform is built from the ground up for security and efficiency, eliminating monthly fees and most standard transaction costs. It's a strong choice for modern businesses, from tech startups to established companies, that value sophisticated digital tools over physical branch access.

What truly differentiates Bank Zero is its advanced, secure functionality designed for teams. The ability to add multiple users with specific, customisable permissions and transaction approval chains is a feature typically reserved for premium, high-cost business accounts. This allows business owners to delegate financial tasks without losing control, making it ideal for companies with several employees managing payments or finances. The focus on zero-fee electronic payments and transfers makes day-to-day digital banking genuinely free.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R0 |

| Eligibility | All registered business types |

| Electronic Payments | Free (EFTs, debit orders) |

| Key Benefit | Advanced user management & permissions |

| Card Swipes | Unlimited, free |

Our Assessment

The primary drawback of Bank Zero is its complete lack of physical infrastructure. Businesses that frequently handle cash for deposits or withdrawals will find this model impractical, as all cash transactions must be done at a retailer like Pick n Pay or Shoprite at a cost. However, for a business that receives payments electronically and pays suppliers via EFT or card, its cost structure is unbeatable. Bank Zero is the future of business banking for digital-native companies that need robust security and team collaboration features without the hefty price tag.

Website: Bank Zero Business Account

9. Mercantile Bank Business Account

Best For: Established SMEs Seeking Personalised Banking Relationships

Mercantile Bank, now a division of Capitec, offers a business account that strikes a balance between affordability and dedicated service. It’s an ideal choice for established small and medium-sized enterprises (SMEs) that have outgrown basic, no-frills accounts and require a more personalised banking relationship. The R65 monthly fee is highly competitive, especially considering it includes access to a dedicated relationship banker.

What sets this account apart is its focus on service for growing businesses. While many low-cost options are purely digital, Mercantile provides a human touch, offering tailored advice and support. This makes it a strong contender for businesses that value expert guidance on financing, forex, and cash flow management but are still searching for one of the cheapest business bank account options that offers more than just the basics. The 24/7 internet banking platform ensures operational efficiency remains high.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R65 |

| Eligibility | All business types (Sole Proprietor, Pty Ltd, etc.) |

| Key Benefit | Access to a dedicated relationship banker |

| Digital Access | 24/7 business internet banking |

| Transaction Fees | Competitively priced per transaction |

Our Assessment

The primary drawback is Mercantile's limited physical branch network, which might be a concern for businesses that frequently handle large cash deposits. However, this is becoming less of a hurdle for companies embracing digital transactions. The real value lies in its service-oriented model, providing support often reserved for premium, high-cost accounts. If your business requires occasional, expert financial guidance without paying exorbitant monthly fees, Mercantile offers a compelling and cost-effective middle ground.

Website: Mercantile Bank Business Account

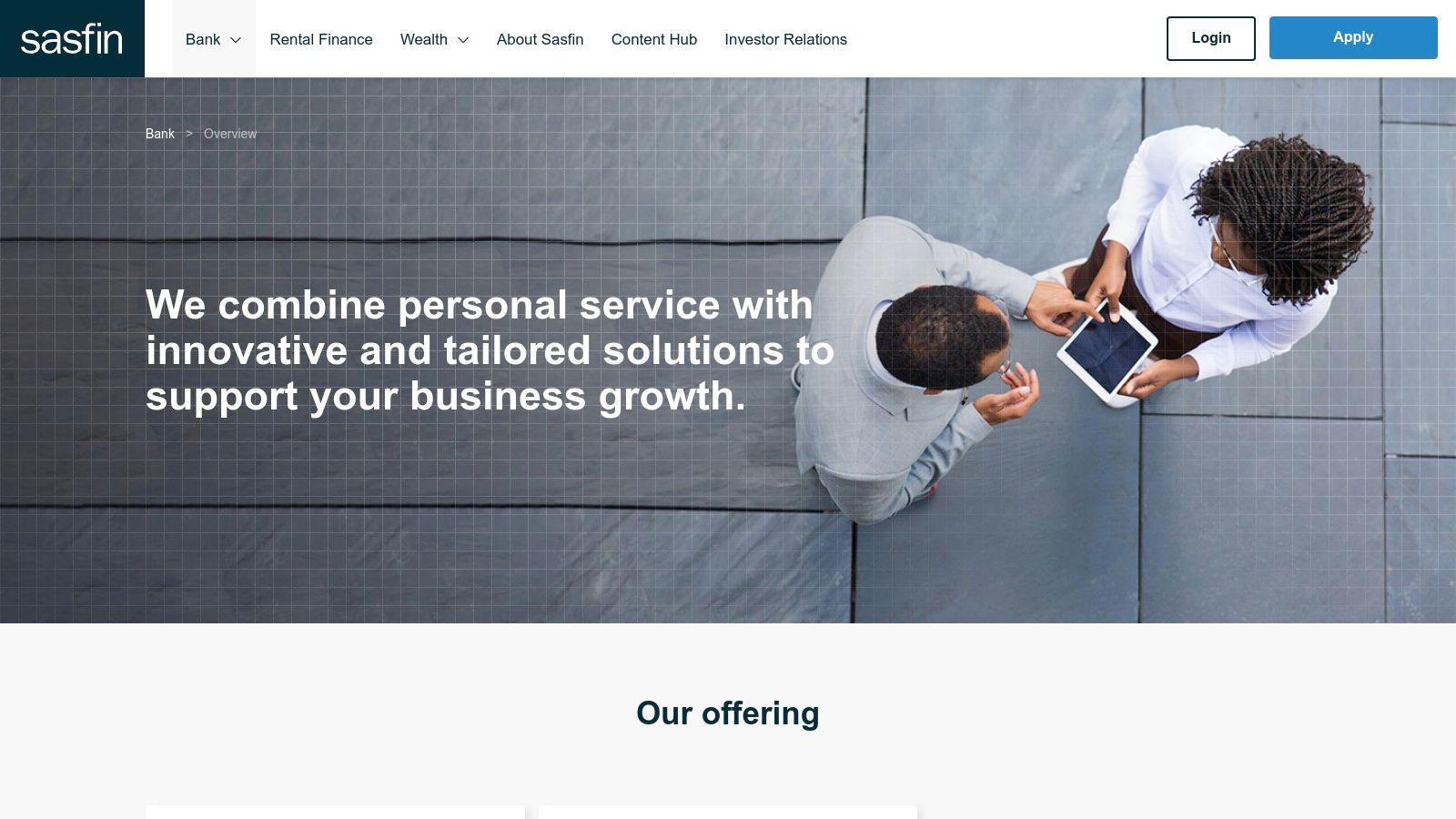

10. Sasfin Business Account

Best For: Established SMEs Needing Integrated Financial Tools

The Sasfin Business Account positions itself not just as a bank account, but as a comprehensive financial management platform. It's tailored for established small to medium-sized enterprises (SMEs) that have moved beyond basic transaction needs and require more sophisticated tools. While not the cheapest business bank account in terms of a monthly fee, its value lies in the bundled services designed to streamline business operations.

What makes it stand out is its digital-first approach combined with powerful integrations. The account seamlessly connects with accounting software like Xero, reducing manual admin and providing a real-time view of your company's financial health. This focus on integrated services makes it an excellent choice for businesses looking to scale and optimise their back-office processes.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R199 (bundled) |

| Eligibility | All business types (Pty, CC, Sole Prop) |

| Card Swipes | Included in bundle |

| Key Benefit | Integration with Xero and other business tools |

| Withdrawals/Deposits | Charged per transaction |

Our Assessment

The primary drawback is the R199 monthly fee, which places it in a higher price bracket compared to zero-fee alternatives. This makes it less suitable for new startups or sole proprietors with very low transaction volumes. However, for a growing business that would otherwise pay separately for accounting software integration and requires access to specialised business loans and asset finance, the bundled fee can represent good value. The account is ideal for businesses that prioritise operational efficiency over achieving the absolute lowest monthly cost.

Website: Sasfin Business Account

11. Discovery Bank Business Account

Best For: Businesses Seeking Integrated Banking and Wellness Rewards

Discovery Bank enters the business banking space with a unique value proposition that ties financial health to its renowned Vitality rewards programme. While not strictly the cheapest business bank account in terms of a zero-fee structure, its value comes from integrated benefits. It appeals to business owners who are already part of the Discovery ecosystem (Health, Insure) and want to consolidate their financial life while earning rewards for prudent financial behaviour.

The account structure is built around a suite of features that go beyond basic transactions. The integration with Vitality Money incentivises good financial habits, such as saving and managing debt, by offering dynamic interest rates and discounts across the Discovery network. This makes it a compelling option for established businesses that can leverage the full spectrum of rewards, potentially offsetting the monthly account fees.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | Varies by package |

| Eligibility | All business types |

| Card Swipes | Included in bundle or pay-as-you-use |

| Key Benefit | Vitality Money rewards for positive banking behaviour |

| Unique Feature | Integrated personal and business banking view |

Our Assessment

The primary drawback is the cost; its monthly fees make it less suitable for startups or businesses purely hunting for the lowest operational cost. The full value is only unlocked if you actively engage with the Vitality Money programme and use other Discovery products. However, for a business owner who values a holistic approach to finance and wellness and can maximise the rewards, the benefits can outweigh the fees. It's less a cheap account and more a value-added financial management tool.

Website: Discovery Bank Business Account

12. Lulalend Business Account

Best For: Businesses Prioritising Fast Access to Working Capital

Lulalend’s offering is a unique entry in the search for the cheapest business bank account because it merges day-to-day banking with its core strength: business funding. The account itself carries no monthly fee, making it an attractive base for SMEs that need a simple transaction account but also anticipate the need for quick-turnaround working capital. This is less a traditional bank account and more a financial hub designed for growth.

Its standout feature is the seamless integration between the transaction account and Lulalend’s revolving credit facility. This structure allows businesses to apply for and access funds directly within their banking environment, simplifying cash flow management significantly. It’s ideal for companies that experience fluctuating income or need to seize inventory or project opportunities without the lengthy processes of traditional bank loans.

Key Features and Costs

| Feature/Fee | Details |

|---|---|

| Monthly Account Fee | R0 |

| Eligibility | All registered South African businesses |

| Card Swipes | Unlimited, free |

| Key Benefit | Integrated access to fast business funding |

| Withdrawals/Deposits | Charged per transaction |

Our Assessment

The primary advantage of the Lulalend Business Account is its specialisation. If your main priority is having an easily accessible credit line for working capital, this account is purpose-built for you. The lack of monthly fees makes it a risk-free choice. However, its main limitation is the narrow scope of its banking services. It doesn't offer the comprehensive suite of tools like foreign exchange, investment options, or complex payment solutions that larger, more established banks provide. It’s an excellent, cost-effective tool for funding-focused businesses but may need to be paired with another account for more diverse banking needs.

Website: Lulalend Business Account

12 Business Bank Accounts: Cost & Features Comparison

| Product | Core Features / Highlights | User Experience & Quality ★★★★☆ | Value & Pricing 💰 | Target Audience 👥 | Unique Selling Points ✨ |

|---|---|---|---|---|---|

| 🏆 Zaro | Real FX rates, zero SWIFT fees, fast transfers | High transparency, enterprise-grade security | Ultra-low FX spread (0.17%), no hidden fees | SA exporters, CFOs, BPOs | Debit cards in ZAR/USD, multi-user access |

| FNB First Business Zero Account | No monthly fee, unlimited free card swipes | Good digital tools | Zero monthly fees | Sole proprietors, startups | Business coaching access |

| Absa Business Evolve Lite | No monthly fee, pay-as-you-use fees | Affordable with dedicated support | Zero monthly fee, fees on usage | Small businesses | Free online banking & NotifyMe |

| Nedbank Startup Bundle | Zero fees 6 months, 20 free digital transactions | Cost-effective for startups | Free first 6 months, then pay-as-you-use | Sole proprietors, private companies | Dedicated banker, SimplyBiz tools |

| Standard Bank MyMoBiz Account | Low monthly fee (R7), digital platforms | Affordable, digital tools | Low monthly fee | Small businesses, entrepreneurs | PocketBiz for card payments |

| Capitec Business Account | Transparent fees, mobile app | User-friendly app | R65/month | Small-medium businesses | Integrated personal & business banking |

| TymeBank EveryDay Business Account | No monthly fee, easy online registration | Simple, digital only | Zero monthly fee | Entrepreneurs preferring digital banks | Earn interest on balances |

| Bank Zero Business Account | No monthly fees, free electronic transactions | Advanced digital features | Completely fee-free | Digital-first businesses | Multi-user approval settings |

| Mercantile Bank Business Account | R65 monthly fee, relationship banker access | Personalized support | Moderate fees | Diverse business types | 24/7 internet banking |

| Sasfin Business Account | R199 bundle, accounting software integration | Comprehensive tools, SME focused | Higher monthly fee | SMEs | Funding & accounting software integration |

| Discovery Bank Business Account | Variable monthly fees, Vitality Money rewards | Rewards incentivize financial health | Fees vary by package | Businesses seeking integrated rewards | Vitality Money program |

| Lulalend Business Account | No monthly fee, quick funding access | Fast funding solutions | Zero monthly fee | SMEs needing funding | Simple online application |

Making the Smartest Choice for Your Bottom Line

Navigating the landscape of business banking in South Africa reveals a crucial truth: the quest for the cheapest business bank account is not a one-size-fits-all endeavour. As we have explored, the definition of ‘cheap’ fundamentally changes based on your business’s unique operational model, transaction volume, and growth trajectory. Your ideal financial partner is the one that aligns most effectively with these specific factors, not just the one with the lowest advertised monthly fee.

For a new startup, a freelancer, or a small local business with straightforward, low-volume transaction needs, the rise of digital-first and challenger banks has been revolutionary. Accounts like the TymeBank EveryDay Business Account or Bank Zero Business Account present compelling zero-fee structures that minimise overheads during critical early stages. Similarly, established banks like FNB, with its First Business Zero Account, have responded with entry-level options that eliminate monthly costs, making them excellent starting points.

Evolving from 'Cheap' to 'Value'

However, as a business scales, the initial appeal of a zero-fee account can become misleading. The true cost of banking often hides in the details of transactional fees. A business processing numerous electronic payments, cash deposits, or point-of-sale transactions might find that an account with a slightly higher monthly fee but more generous free transaction bundles, such as those offered by Absa Business Evolve Lite or the Nedbank Startup Bundle, delivers better overall value.

The most significant shift in this cost-benefit analysis occurs when a business engages in international trade. For South African export companies, BPOs, and businesses with global clients, the seemingly minor percentage points on foreign exchange (FX) markups and the high flat fees on cross-border payments can accumulate into a substantial operational expense. This is where traditional 'cheap' accounts falter, as their international transaction costs can quickly erode any savings made on local banking.

Aligning Your Account with Your Ambition

Choosing the right account requires an honest assessment of your business today and a clear vision for where you want it to be tomorrow. Consider these final points before making your decision:

- Analyse Your Transactions: Scrutinise your last six months of banking statements. Where does your money go? Are you dominated by EFTs, cash deposits, or international transfers? Match your highest-volume activities to the account that charges the least for them.

- Factor in Future Growth: If you plan to start exporting or hiring international talent within the next year, factor in the costs of global payments from day one. Choosing a specialised service now can prevent costly and disruptive migrations later.

- Look Beyond the Fee: Consider the value of integrated tools. Do you need invoicing software, payroll integration, or access to business funding? Sometimes a slightly more expensive account that includes these features, like offerings from Sasfin or Lulalend, can save you money on separate third-party software subscriptions.

Ultimately, selecting the cheapest business bank account is a strategic decision that directly impacts your profitability. It's about finding an intelligent financial solution that minimises friction and cost, allowing you to focus your resources on what truly matters: growing your business.

Ready to eliminate the hidden costs of international trade and truly optimise your bottom line? Discover how Zaro offers transparent, low-cost foreign exchange and global payment solutions designed for ambitious South African businesses. Stop overpaying on cross-border transactions and see how a specialised platform can be the smartest choice you make.