At its core, an international money transfer is simply the process of sending money from one country to another using a specialised financial service. For a South African business, this could mean paying a supplier in China, getting paid by a customer in the UK, or managing salaries for a remote team in Europe.

Why Mastering Global Payments Is a Game-Changer for Growth

If your South African business has global ambitions, sending and receiving money across borders isn't just another administrative chore—it's a vital link in your operational chain. The way you handle these international payments can directly boost your profitability, strengthen supplier relationships, and sharpen your competitive edge.

Get it wrong, and you create friction. Get it right, and you unlock a serious advantage.

Think of it like this: slow, costly, or unreliable payments are like roadblocks in your financial workflow. They can hold up shipments, create tension with your partners, and quietly erode your profits with one unexpected fee after another.

The Real-World Hurdles You're Up Against

So many businesses run into the same old frustrating problems. The traditional ways of sending money overseas are often packed with hidden costs and baffling processes. These aren't just small annoyances; they're real financial and operational risks.

Here’s what that typically looks like:

- Surprise Fees: You send a payment, but along the way, intermediary banks take a slice, and the receiving bank might charge its own fee. None of this is clear from the start.

- Frustrating Delays: A transfer can take days to actually land, leaving both you and your partners waiting. This kind of uncertainty is terrible for cash flow.

- Confusing Regulations: Trying to make sense of South Africa's exchange control rules can feel like a full-time job, creating genuine compliance headaches.

- Poor Exchange Rates: Many providers hide their profit in the exchange rate they offer you. This markup means you lose a bit of money on every single transaction, often without even knowing it.

When you turn your international payment process from a business headache into a strategic asset, you open the door to real growth. It’s all about making your financial operations as lean and efficient as the rest of your company.

Ultimately, mastering international money transfers is about taking back control of your global cash flow. It’s a shift from being reactive—just sending money and hoping it gets there—to building a proactive strategy. With the right partners and tools, you can make cross-border payments faster, cheaper, and far more predictable, building a solid foundation to expand your business internationally.

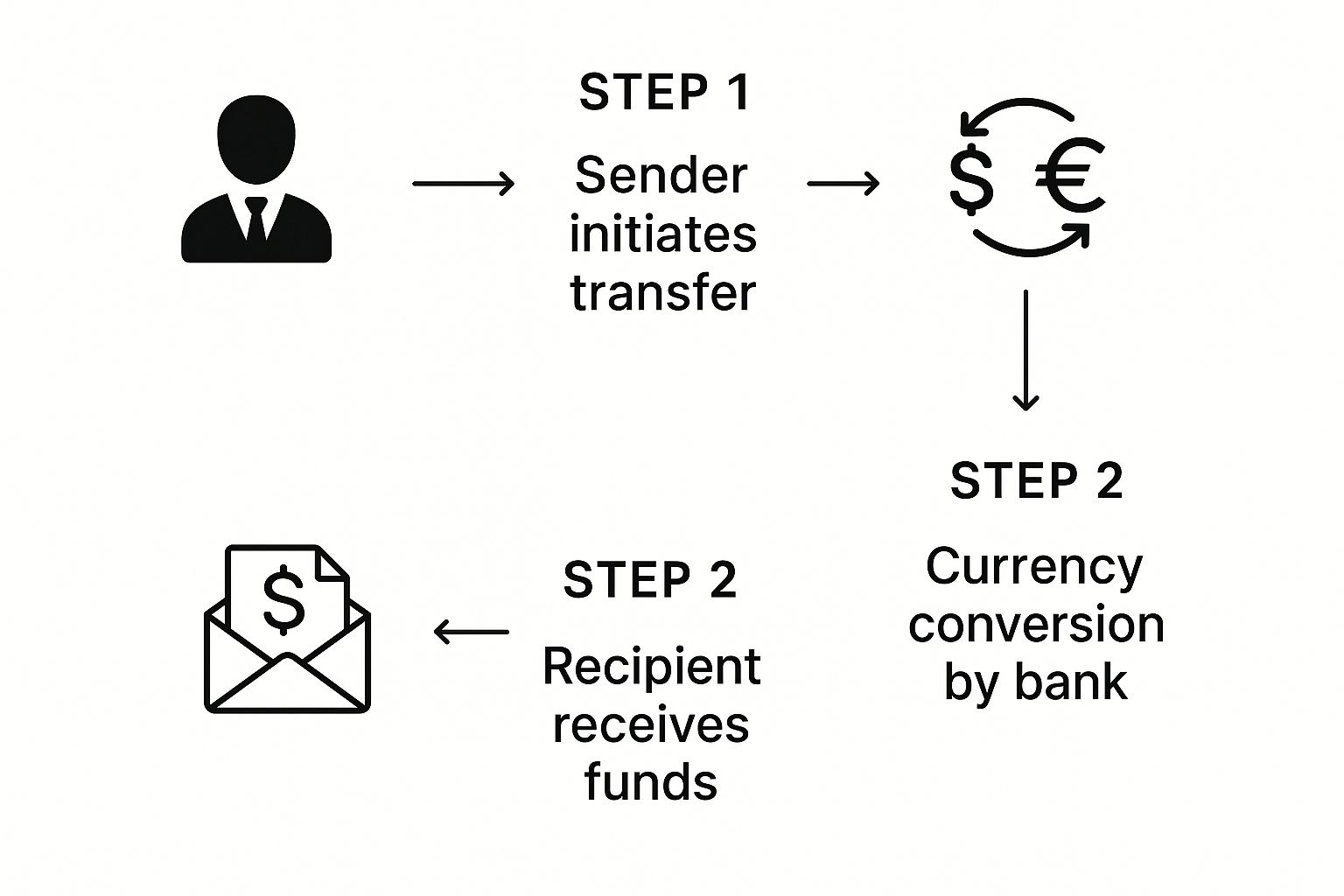

How Your Money Actually Travels Across Borders

Ever wondered what happens after you click "send" on an international payment? It's easy to picture your Rands zipping across the globe like an email, landing directly in your supplier's account. The reality, at least with traditional banking, is a lot less direct. Think of it less like a direct flight and more like a long-distance relay race.

This old-school process relies on a chain of banks to get your money from point A to point B. If your bank in South Africa doesn't have a direct link to the recipient's bank in Germany, for example, it has to pass the funds through one or more correspondent banks. Each handoff in this chain adds time, creates opportunities for errors, and, importantly, adds fees that eat into the amount you sent.

This infographic breaks down the typical steps involved.

As you can see, the multiple stages, especially currency conversion and intermediary processing, are where delays and costs start to stack up.

The Role of SWIFT and Correspondent Banking

The messaging system that powers this global relay race is called SWIFT (Society for Worldwide Interbank Financial Telecommunication). It's a common misconception that SWIFT actually moves money. It doesn't. Instead, it sends secure payment instructions between banks. You can think of it as the postal service of the banking world—it delivers the message that says, "Please transfer this amount from this account to that one."

So where does the money move? The actual funds are settled between special accounts that banks hold with each other, known as nostro and vostro accounts. A nostro account is basically 'our money with you,' while a vostro is 'your money with us.' This network of accounts allows banks to clear payments without having to physically ship cash across borders.

The big problem with this traditional system is its dependence on these middlemen. Each bank in the chain is a potential bottleneck, adding its own processing time and service fee. This is precisely why a simple transfer can take 3-5 business days and arrive with less money than you thought you sent.

Modern Fintech: A More Direct Route

This is where modern fintech platforms have completely changed the game. They’ve looked at this slow, expensive relay race and designed a more direct route. Instead of passing your money through multiple hands, they operate more like a direct flight.

How do they do it? Many maintain their own pools of local currency in different countries. When you need to pay a supplier in the US, you pay into the fintech’s local account here in South Africa. They then pay your supplier out of their local account in the US. This clever internal settlement process bypasses the SWIFT network and its correspondent banks entirely.

This approach brings some serious benefits:

- Speed: Transfers are often completed in hours, sometimes even minutes, not days.

- Cost Savings: By cutting out the intermediary bank fees, the total cost of the transaction drops dramatically.

- Transparency: You know exactly how much your recipient will get from the start. No more nasty surprises from hidden fees.

Getting your head around this fundamental difference is vital for any South African business trading globally. The method you choose for your international money transfers has a real impact on your cash flow, supplier relationships, and bottom line. To see how money can move more efficiently, it's worth exploring these innovative cross-border payment solutions. By choosing a more direct path, you can transform a slow, expensive headache into a fast, reliable, and cost-effective part of your business.

Uncovering the True Cost of Sending Money Abroad

The fee you see upfront when making an international money transfer is rarely the full story. It's just the tip of the iceberg. Lurking beneath the surface are hidden charges and poor exchange rates that can seriously inflate the real cost of moving your money across borders. For any South African business, getting a handle on these total costs is non-negotiable for protecting your profit margins.

Think of it like booking a budget flight. The ticket price looks fantastic, but by the time you've added luggage, picked a seat, and paid for a coffee, the final amount is far from what was first advertised. Global payments work much the same way, and the biggest hidden cost is almost always baked into the exchange rate.

The Hidden Cost of Exchange Rate Markups

More often than not, the single biggest expense in an international transfer isn't the flat fee you're quoted. It’s the exchange rate markup. This is the gap between the ‘real’ mid-market exchange rate—what banks use to trade currencies among themselves—and the less attractive rate offered to you, the customer.

That difference, often called a 'spread', is pure profit for the provider. A seemingly tiny markup of 2-4% can translate into huge losses, especially when you're dealing with large transaction volumes. For instance, on a R200,000 payment to a US-based supplier, a 3% markup means R6,000 vanishes from your bottom line before any other fees are even touched.

Many providers will shout about "zero commission" or "low-fee" transfers, but they're often just hiding their profit in an inflated exchange rate. Always check the rate you’re offered against the live mid-market rate to see what you're really paying.

This common practice makes it incredibly tricky to compare services on a like-for-like basis, because the provider with the lowest advertised fee could easily be the most expensive overall.

Beyond the Rate: Other Fees to Watch For

While the exchange rate markup is the main offender, a whole host of other fees can pop up along the payment's journey, slowly chipping away at the amount your recipient eventually gets.

Keep an eye out for these:

- Intermediary Bank Fees: If your payment travels through the traditional SWIFT network, the correspondent banks that help it along the way can—and often do—deduct their own processing fees directly from your funds.

- Receiving Bank Charges: The bank on the other end might also levy a charge just for processing and depositing an incoming international payment. It’s another cost you might end up covering.

- Amendment Fees: Made a typo in the beneficiary’s details? Banks are known to charge hefty fees to fix or recall a payment that’s already in the system.

These small, individual charges stack up, creating a noticeable difference between the amount you sent and the amount that lands. That’s why figuring out the 'all-in' cost is so critical for financial planning.

Calculating Your All-In Cost of Transfer

To get a true picture of what you're paying, you have to look past the initial quote. The all-in cost is a simple calculation that combines the upfront transfer fee with the hidden cost of the exchange rate markup. It’s the only way to genuinely compare different providers.

The formula is straightforward: Upfront Fee + (Mid-Market Rate - Offered Rate) x Transfer Amount.

By running this calculation for each provider you're considering, you can instantly see which service offers the best value for your business. This kind of transparency is the foundation of a smart international payment strategy.

To put this into perspective, let's look at how the different methods stack up.

Comparing International Money Transfer Methods and Costs

The table below breaks down the most common ways to send money internationally, highlighting how their costs, speeds, and ideal use cases differ for South African businesses.

| Transfer Method | Upfront Fee | Exchange Rate Markup | Typical Speed | Best For |

|---|---|---|---|---|

| Traditional Banks | R250 - R600+ | 2% - 5% | 3-5 Business Days | Large, infrequent corporate transfers where convenience is prioritised over cost. |

| Online Money Transfer Services | R0 - R150 | 0.5% - 2% | 1-2 Business Days | Small to medium-sized payments where cost and speed are balanced. |

| Fintech Payment Platforms (like Zaro) | R0 | 0% (Mid-Market Rate) | Same Day / Next Day | Businesses of all sizes needing cost-effective, fast, and transparent recurring payments. |

As you can see, platforms that give you access to the real mid-market rate immediately eliminate the largest and most deceptive cost tied to international money transfers. By partnering with a provider that believes in a transparent pricing model, South African businesses can stop overpaying and start redirecting that capital back into growing the company.

Navigating South African Exchange Control Regulations

For any South African business trading globally, compliance isn't just another box to tick. It’s the very bedrock of every international transaction you make. The rules governing international money transfers are set out by the South African Reserve Bank (SARB), and getting to grips with them is non-negotiable. One misstep can lead to serious penalties, frustrating payment delays, and even legal headaches.

Think of exchange control regulations as the official rulebook for moving money across our borders. They’re in place to monitor the flow of capital, protect the national economy, and maintain financial stability. They might seem intimidating at first, but once you understand the basic principles, they become a lot less complicated.

At its core, it's all about transparency. SARB needs to know the "who, what, where, and why" behind every cross-border payment to prevent illegal financial activities and keep an accurate pulse on the economy.

The Role of the South African Reserve Bank

The SARB is the ultimate authority overseeing all foreign exchange transactions in the country. However, it doesn't handle every single transfer itself. Instead, it delegates the day-to-day administration to commercial banks, which are known as Authorised Dealers. This means that whenever your business needs to send or receive money internationally, you'll almost always be working through one of these approved institutions.

This system creates a clear, traceable path for every rand that crosses our borders. Authorised Dealers are on the front line, responsible for checking that each payment is for a legitimate reason and is backed by the right paperwork. They essentially act as the gatekeepers, making sure everyone plays by the rules.

Understanding Balance of Payments Reporting

A crucial part of this system is Balance of Payments (BOP) reporting. Every time your business makes or receives an international payment, your bank has to report it to the SARB using a specific category code. This isn't just about red tape; it's a vital cog in the country's economic machinery.

These BOP codes simply classify the nature of the transaction. For example:

- Importing goods from a supplier in Germany.

- Paying for a software subscription from a company in the US.

- Receiving payment for exports you’ve sent to a client in Kenya.

- Making a royalty payment or bringing profits back home.

Getting this classification right isn't optional. It feeds critical data to the SARB about South Africa's trade balance and overall economic health, ensuring all international money transfers are properly accounted for.

Why Documentation Is Non-Negotiable

Because every single transaction needs a legitimate purpose, you will always be asked for supporting documents. This is the step where many businesses get tripped up, leading to frustrating delays. Knowing what you need from the get-go can make all the difference.

The most common requirement is a commercial invoice. It needs to spell out the transaction details clearly—who the buyer and seller are, what goods or services are involved, and the total value. For other payments, you might need to provide a contract, a loan agreement, or other official documents.

Think of it this way: The BOP code is your declaration of what you're doing. The supporting documents are the proof. When your paperwork is clear and correct, the Authorised Dealer can give your payment the green light without any fuss.

This thorough oversight is part of a bigger picture. The South African Reserve Bank has been vocal about the need to improve our cross-border payment systems to cut down on high costs and long waits. As a member of the G20, South Africa is part of a global push to make payments cheaper, faster, and more transparent—a goal that relies on a strong regulatory foundation. You can read more about SARB's vision for cross-border payments in Sub-Saharan Africa.

The Risks of Getting It Wrong

Let's be clear: trying to sidestep exchange control regulations is a risky game. The consequences can be severe, from heavy fines right through to having your business assets frozen. Beyond the direct financial hit, failed or delayed payments can seriously damage your reputation with international suppliers and customers, disrupting your entire supply chain.

But here’s the good news—compliance doesn't have to be a nightmare. By partnering with a financial provider that understands the ins and outs of South African regulations, you can turn this complex task into a simple, automated part of your process. The right platform will guide you on documentation, handle the BOP reporting, and ensure every payment ticks all the compliance boxes, freeing you up to focus on what you do best: growing your business.

The Future of Cross-Border Payments in Africa

The way African businesses send and receive money across borders is about to change, and it’s a big deal. For years, we’ve been stuck with slow, expensive payment rails that often sent money on a world tour—routing payments through banks in Europe or North America, even just to trade with a neighbouring country. This outdated model is finally being dismantled by a wave of African-led financial technology.

This isn’t just about making payments faster. It’s about building a more connected, self-sufficient African economy. One where a South African business can trade with a partner anywhere on the continent as easily as they do locally. The goal is to tear down the old financial roadblocks and build direct, efficient payment highways in their place.

A New Era of Intra-African Trade

At the heart of this shift is a simple but powerful idea: African trade should be settled in African currencies, using African systems. For too long, a South African business paying a supplier in Nigeria would watch its Rands get converted to US Dollars, sent to a US bank, and then converted again into Naira. Every step added delays and tacked on costs, making trade on our own continent far more complicated than it needed to be.

This is where incredible new initiatives are stepping in, creating massive growth opportunities for businesses ready to expand their footprint across Africa.

The core principle is straightforward: if you are trading within Africa, your payments should stay within Africa. This shift not only slashes costs but also strengthens regional economic ties and cuts down our reliance on external financial systems.

By keeping capital flowing within the continent, these new systems are forging a more resilient and integrated marketplace. It's a win-win for everyone, from small exporters to large corporations.

The Pan-African Payment and Settlement System

One of the most exciting developments is the Pan-African Payment and Settlement System (PAPSS). This platform was built specifically to cut non-African banks out of the loop for intra-African trade. It allows businesses across the continent to pay for goods and services in their own local currencies, with settlement happening almost instantly.

Think about it: your business in Johannesburg needs to pay an invoice to a partner in Ghana. Instead of a multi-day headache involving US Dollar conversions, PAPSS enables a direct transaction. You pay in ZAR, and your partner receives Ghanaian Cedi almost immediately. This is more than just a convenience; it’s a total overhaul of the continent's financial architecture.

Regional initiatives like PAPSS are finally getting recognised for their power to dramatically reduce the costs and delays of international money transfers coming out of South Africa and other African nations. First launched in West Africa, the system makes instant payments in local currencies possible, with the African Export-Import Bank (Afreximbank) guaranteeing final settlement. This makes it a critical tool for smoother trade. You can learn more about the impact of these payment infrastructures and what they mean for the future.

What This Means for Your Business

For a South African business, this future brings real, tangible benefits that hit your bottom line and improve how you operate. The advantages are clear and compelling.

- Drastically Reduced Costs: By cutting out correspondent bank fees and multiple currency conversions, you can save a significant amount on every single transaction.

- Faster Settlement Times: Payments that once took days can now be settled in hours or even minutes. This improves your cash flow and builds stronger relationships with suppliers.

- Reduced FX Risk: Trading directly in local currencies helps protect your business from the volatility that comes with converting funds into and out of major global currencies like the US Dollar.

- Simplified Operations: A more direct payment process means less admin, fewer things that can go wrong, and far more predictability for your finance team.

This evolution is creating a single African market for payments. For South African businesses, it’s becoming easier and more profitable than ever to thrive right here on the continent.

Choosing the Right Partner for Your Global Payments

Getting to grips with the costs, rules, and general workings of international money transfers is one thing. But turning that knowledge into a smart business decision is where it really counts. Choosing the right financial partner will directly impact how smoothly your business runs and, ultimately, how much money you keep.

For any South African business trading globally, this isn't just about hunting for the lowest fee. It's about finding a platform that truly understands and solves the unique headaches of cross-border payments.

Think about it. You need to pay a crucial supplier in Europe. Going through your bank often means a sluggish process, an exchange rate that works against you, and a whole lot of guesswork about when the money will actually land. This kind of friction doesn't just slow you down; it can chip away at the trust you've built with your partners.

A modern payment partner flips this entire script. They turn a stressful, unpredictable task into a straightforward, almost boring, part of your day-to-day operations. Platforms like Zaro were built specifically to tackle these pain points, offering clear fee structures, the real mid-market exchange rate, and built-in compliance tools that clear the path to real savings and slicker operations.

From Theory to Real-World Application

Let's put this into a practical context. Imagine paying an international freelancer or getting paid by a client overseas. With the right partner, the whole process becomes almost effortless.

Instead of wrestling with clunky banking portals and bracing for surprise fees, you get a clean, central dashboard. From here, you can fire off payments in minutes, see exactly where your money is in real-time, and handle all the necessary compliance reporting for the South African Reserve Bank without breaking a sweat. If you're looking for what a modern, integrated solution can do, looking at a comprehensive guide to a system like the Shopify Payments gateway can offer some great perspective.

This shift gives you a new level of control, turning international money transfers from a reactive chore into a powerful tool for your business.

Key Factors to Evaluate in a Payment Partner

As you start comparing your options, zero in on the things that will make a tangible difference. You're not just looking for a transaction service; you're looking for a genuine partner.

Here’s what to look for:

- Transparent Pricing: Are you getting the real mid-market exchange rate without hidden markups? This is the number one way you'll cut costs.

- Speed and Reliability: How fast do payments actually arrive? A platform that sidesteps the old, slow SWIFT network can settle funds in hours, not days. That’s a game-changer for your cash flow.

- Compliance Automation: Does the platform help you manage your SARB reporting? This can save you a mountain of admin time and cut down on compliance risks.

- Security and Control: Look for robust security like multi-user permissions and detailed audit trails. You need to have complete, confident oversight of your company’s finances.

At the end of the day, the right partner does more than just move your money. They provide a secure, efficient, and clear financial foundation that helps your business grow, letting you compete on the world stage with confidence.

Common Questions About International Money Transfers

When you're dealing with international money transfers, it’s natural for questions to pop up. You're trying to find that sweet spot between cost, speed, and keeping everything above board. Getting clear answers is the first step to building a global payment strategy that actually works for your business.

Let's break down some of the most common questions we hear from South African businesses. Answering these will help you piece together the puzzle and make much smarter financial moves.

What Is the Cheapest Way to Send Money Internationally from South Africa?

Finding the cheapest option means looking at the whole picture, not just the advertised transfer fee. Many businesses default to their bank, but that's often one of the priciest routes. Why? Their costs are usually bloated by poor exchange rates and a string of hidden fees from intermediary banks.

The most cost-effective way is almost always through a provider that gives you the real mid-market exchange rate. Fintech platforms and dedicated transfer services were created specifically to bypass these extra costs. The trick is to always calculate the total cost: that’s the upfront fee plus whatever you lose to the exchange rate markup.

Here’s the bottom line: a low fee is meaningless if you’re losing 3-5% on a bad exchange rate. Your priority should be finding providers who are transparent and offer mid-market rates. That's where the real savings are.

How Long Do International Money Transfers Usually Take?

Transfer times can be all over the map, from just a few minutes to several business days. It all comes down to the payment network being used to move your money.

- Traditional SWIFT Transfers: If you're sending money through the old-school banking system, expect it to take 3-5 business days. The payment has to hop between several correspondent banks, and each stop adds time.

- Modern Payment Platforms: On the other hand, newer fintech solutions often use their own network of local accounts to move money, which can land a payment in under 24 hours. In many cases, it’s practically instant.

For a business, that time difference is huge. Faster payments mean better cash flow, happier suppliers, and less time spent wondering where your money is.

What Documents Do I Need for a Business Transfer from South Africa?

Every international payment leaving South Africa has to meet the South African Reserve Bank (SARB) regulations, which means you need the right paperwork to prove it’s a legitimate transaction.

The most common document you’ll need is a commercial invoice. It needs to clearly show what goods or services you're paying for, who the supplier is, and the total amount. Depending on the reason for the payment, a formal contract or another type of agreement might be required. Using a platform with built-in compliance can make this part much less of a headache, ensuring all your international money transfers tick the right legal boxes.

Ready to take the complexity out of your global payments? Zaro offers South African businesses access to real exchange rates, zero hidden fees, and lightning-fast settlement times. Stop overpaying and start optimising your international money transfers today.