If you've ever felt the sting of a bad exchange rate or surprise fees when trying to buy US dollars, you're not alone. It’s a common frustration for South Africans. The old-school methods we’ve relied on for years often come with murky charges and lousy rates that quietly chip away at your money. Thankfully, there's a much smarter way to do it now.

Why Your Old Forex Method Is Costing You

For too long, buying dollars meant a trip to the bank, a mountain of paperwork, and just accepting whatever exchange rate they decided to give you that day. It's a system from another time, and frankly, its inefficiencies are now hitting your pocket directly.

Let’s say you’re planning a trip overseas. You do your homework, budget based on the rate you see on Google, but when you get to the bank, their rate is way off. Then they tack on "admin" or "service" fees you never saw coming. Before you know it, you're walking out with far fewer dollars than you'd planned for.

The Hidden Costs You Don't See

The core of the problem is a total lack of transparency. Big financial institutions often bake their profit margin right into the exchange rate they offer you. This isn’t the real "mid-market" rate—the one you see online, which is the true halfway point between what buyers and sellers are paying on global markets. That difference, or "spread," might only look like a few cents per dollar, but it adds up incredibly fast.

And it’s not just about travel. What about paying for international software subscriptions like Adobe or Microsoft 365? Every single month, those recurring US Dollar payments are getting hit by your bank's inflated, ever-changing rates.

The real cost isn't the small fee you might see on a statement. It’s the value you lose from a bad exchange rate. A 3-5% markup on the rate itself is often far more expensive than any flat transaction fee, especially when you’re dealing with larger sums of money.

Dealing with a Wildly Fluctuating Rand

The rand's volatility makes getting a good deal on currency conversion even more critical. We all know the ZAR-to-USD rate can swing wildly based on what’s happening at home and around the world.

If you look back, the rate has gone from single digits to nearly R20 to the dollar. Not long ago, it hit a record high of around 19.93 ZAR per USD, mostly driven by economic jitters. This just goes to show how much outside events affect what you actually pay for dollars. If you’re interested, you can dive into historical currency trends to see these patterns for yourself.

This is where modern digital platforms change the game completely. They give you access to real-time exchange rates with clear, minimal fees, putting you back in the driver's seat. Instead of just taking whatever rate you're given, you can watch the market and choose the best moment to convert your rands, making sure your money goes as far as it possibly can.

Getting Your Digital Forex Account Set Up

Making the move to a modern currency platform like Zaro is a world away from the old-school, paperwork-heavy process we've all come to dread. There are no queues and no stacks of forms. The entire thing happens on your phone or computer, and it’s genuinely designed to get you from zero to buying dollars in just a few minutes.

You’ll start by downloading the app and putting in the basics – your name, email, and a strong password. That part’s quick. The next bit, verification, is where the real security kicks in, and it's essential for keeping your account safe.

Acing the FICA Verification

If you’ve ever opened a bank account in South Africa, you’ll know all about FICA. It’s a legal must-have to confirm who you are and to clamp down on financial crime. The good news is that digital platforms have made this a breeze, but a little prep goes a long way.

Have these two documents handy:

- Proof of Identity: A sharp, clear photo of your green ID book or smart ID card. Make sure all four corners are in the shot and there's no glare from the lights.

- Proof of Address: A recent utility bill or bank statement – usually no older than three months – that clearly shows your name and physical address.

A common trip-up? A blurry photo or a document that’s out of date. My personal tip is to place your ID on a plain, dark surface to take the photo and download a fresh PDF of your utility bill straight from your provider’s website. This helps you avoid any quality issues that might slow down your approval.

FICA isn't just a box-ticking exercise; it's there to protect you. A platform that takes verification seriously is showing you they're committed to security. Think of it as building a digital fortress around your money right from the start.

Finding Your Way Around the Platform

Once you get that "approved" notification, take a couple of minutes to click around the app and get a feel for it. It's built to be intuitive, but knowing the lingo will help you move your money with confidence. The first thing you'll probably see is a dashboard with your different currency "wallets"—one for ZAR and another for USD.

Get familiar with these key areas:

- Fund or Deposit: This is your starting point. It’s where you'll find the banking details needed to EFT Rands into your Zaro account.

- Convert or Exchange: The main event! This is the tool you’ll use to swap your Rands for Dollars at the live market rate.

- Withdraw or Send: When it's time to move your money out, this is where you’ll go, whether you're sending it to your own bank account or making an international payment.

Nailing these basics means you’re not just blindly following instructions; you're actually in the driver's seat. It gives you the confidence to make that first transaction, knowing exactly where everything is and what to expect.

Getting Your Rands Ready for Conversion

Once you’re all set up, the first thing you'll want to do is get your Rands into your Zaro wallet. The whole process is designed to feel as familiar as paying a friend or a bill, giving you full control from start to finish.

The easiest way is a simple Electronic Funds Transfer (EFT) directly from your South African bank account. When you open the Zaro app, you'll see your unique deposit details. Just copy those over and make a standard payment from your banking app, like you would for any other beneficiary.

Here’s a small but crucial tip: always, always include your unique reference number. This little detail is what allows the system to automatically link the deposit to your specific Zaro wallet. If you forget it, the funds will still arrive, but it’ll need a manual allocation, which can slow things down.

From Funding to Buying Dollars

With your Rands safely in your account, it's time for the main event: converting them into US Dollars. This is where you really see the difference between old-school banking and a modern platform. You’re no longer stuck with whatever "rate of the day" a bank teller gives you. Instead, you get a front-row seat to the live currency market.

You can actually watch the ZAR/USD exchange rate fluctuate in real-time right inside the app. This transparency is a game-changer because it lets you be strategic. You can monitor the market and pounce when the rate looks good to you, rather than just accepting a fixed quote.

Considering how much our currency can swing, this feature is incredibly useful. For instance, over a recent eight-month period, the Rand went on a rollercoaster ride, hitting a high of 19.757 ZAR per USD at one point, while the average hovered around 17.993. Being able to see these movements gives you the power to act when the rate is in your favour. If you’re interested in the data, you can explore more on historical ZAR to USD exchange rate trends to get a feel for the patterns.

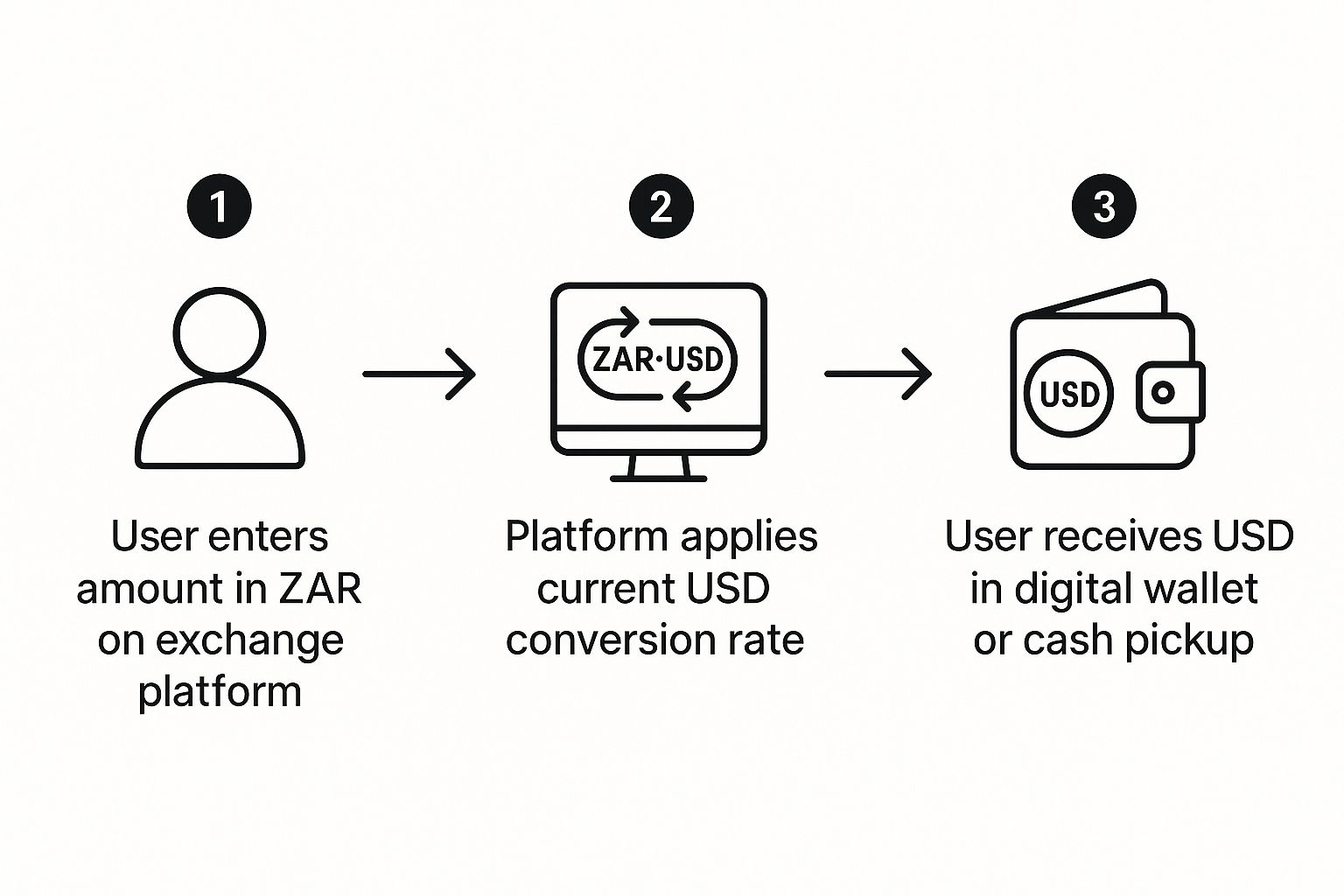

A Real-World Example: Paying an Invoice

Let's walk through a practical scenario. Say you need to pay an overseas supplier and want to convert R15,000 into US Dollars.

At a traditional bank, you'd be quoted a rate that often has a hidden markup baked in. You wouldn't know the exact dollar amount hitting the supplier's account until after the fact, once all the various fees are deducted. With a platform like Zaro, you see everything upfront.

This is the simple flow of how you'd turn your Rands into Dollars.

As you can see, there’s no guesswork involved. You know exactly what you're getting before you commit.

The steps are dead simple:

- You type R15,000 into the conversion tool.

- The live exchange rate is applied instantly.

- You see the final USD amount you’ll receive, down to the last cent.

The fee structure is also laid out clearly—no nasty surprises. Before you even think about hitting "confirm," you see precisely what the service costs and exactly how many dollars will land in your USD wallet.

The real benefit here is certainty. Seeing the live rate and the final dollar amount upfront lets you make informed financial decisions. It completely removes the stress of hidden costs and ensures the amount you budgeted for is the amount you actually get.

Using Your Dollars for Global Transactions

Getting a great rate when you buy dollars with your rands is a fantastic start. But the real win comes when you can actually use those dollars internationally without getting stung by more fees. This is where your new USD balance goes from being a number on a screen to a practical tool for your global life.

The simplest way to start spending is with a virtual card linked directly to your USD balance. It’s essentially a debit card for your dollar wallet, perfect for those international online payments.

Spend Globally, Pay in Dollars

Think about all those international subscriptions. If you run a small business, you’re likely paying for software like Adobe Creative Cloud, a CRM, or web hosting. Before, each monthly payment was a bit of a gamble, subject to your local bank's not-so-great ZAR to USD conversion rate on the day, plus any hidden charges.

When you use a dedicated USD virtual card, you sidestep that entire problem. You're paying in dollars, directly from your dollar balance.

What does this actually mean for you?

- No more nasty surprises. If the invoice says $99, your account is debited for exactly $99. The price you see is the price you pay.

- Clean and simple bookkeeping. All your international expenses are already recorded in USD, which makes reconciling your accounts a breeze.

- Budgeting you can count on. You can plan your overseas spending with real confidence, knowing your costs won't bounce around with the daily exchange rate.

Using your USD balance directly isn't just a convenience—it's a smart financial strategy. You avoid the "death by a thousand cuts" from small conversion fees that traditional banks charge on every single international card payment. Over a year, those savings really start to add up.

Moving Your Money Where It Needs to Go

Of course, it’s not all about online shopping and subscriptions. Sooner or later, you’ll need to send those dollars somewhere else. Maybe you’re paying an international supplier, transferring funds to an overseas bank account, or even pulling the money back into your South African ZAR account.

Initiating a transfer from your USD wallet is designed to be straightforward. You’ll get a clear breakdown of any costs and see the estimated arrival time before you commit.

For example, sending dollars to a US-based bank account is a common need for many businesses and freelancers. With a service like Zaro, the fee structure is transparent. You know precisely what the recipient will get before you even hit 'send'.

This kind of clarity is crucial. It means you can pay international contractors or settle invoices knowing the full, expected amount will arrive without a chunk being shaved off by surprise intermediary bank fees. It turns what was once a complex, anxious process into a predictable part of your financial workflow.

A Smarter Way to Buy Your Dollars

Getting your Rands converted is one thing, but turning that simple transaction into a smart financial move? That’s where the real magic happens. It’s about moving beyond just swapping currencies when you have to and adopting a more calculated approach. This subtle shift can seriously stretch the value you get from every single Rand you convert.

Basically, you stop being reactive and start being proactive. Instead of rushing to convert Rands only when a payment is due, you learn to look ahead, anticipate your needs, and pull the trigger when the market is smiling on you.

Reading the Market to Time Your Conversion

First things first, you need to get your head around the difference between the mid-market rate and the rate your bank gives you. The mid-market rate is the ‘real’ one—the midpoint between what buyers are paying and sellers are asking on the global markets. You'll almost never get this rate from a traditional bank. Instead, they add their own markup, or "spread," which is how they make their profit.

Modern digital platforms, on the other hand, get you much, much closer to that real-time mid-market rate.

A really clever approach is to keep an eye on this rate. You don't need to become a full-blown forex trader, but just watching the trends can make a massive difference. A great tip is to set up rate alerts in your currency app. These can ping you when the ZAR strengthens against the USD, letting you know it’s a good time to act. This one small habit could save you hundreds, if not thousands, of Rands on bigger conversions.

Imagine setting an alert to notify you the moment the rate dips below R18.50 to the dollar. That’s your signal—a potentially perfect time to convert the funds you’ve set aside for that overseas holiday or a future investment.

Understanding What Your Conversion Really Costs

To make genuinely smart decisions, you have to see the full picture of the costs involved. Hidden fees and chunky markups on the exchange rate can quietly eat away at your money. It’s so important to compare your options with total transparency.

For those managing larger sums, weaving efficient currency exchange into your overall financial strategy is non-negotiable. You can explore more advanced strategies in financial planning for high-net-worth individuals to ensure every part of your wealth is working as hard as it can for you.

To see what I mean, let’s put the costs side-by-side.

Comparing Digital Platform and Traditional Bank Forex Fees

Here’s a look at the typical costs for converting Rands to Dollars. It really pulls back the curtain on the hidden fees you might be paying without even realising it.

| Feature | Modern Digital Platform | Traditional South African Bank |

|---|---|---|

| Exchange Rate | Offers the near-real mid-market rate with a minimal, transparent markup. | Provides a consumer rate with a significant, often hidden, spread of 3-5%. |

| Transfer Fees | Low, flat fees that are clearly stated before you confirm the transaction. | Can include admin fees, service fees, and often high SWIFT fees for international transfers. |

| Transparency | All costs are shown upfront, so you know the exact amount you’ll receive. | Fees can be opaque and deducted at various stages, making the final amount uncertain. |

This comparison makes it pretty clear where the real costs lie.

The biggest "fee" you'll ever pay is often hidden inside the exchange rate itself. A platform offering a better rate will almost always save you more money than one that shouts about low transfer fees but quietly pads its margin in a poor rate.

By using simple tools like rate alerts, getting wise to the real costs, and picking a platform that values transparency, you put yourself in control. You stop just buying dollars and start managing your currency strategically. It’s an approach that makes sure your hard-earned Rands go a whole lot further when you spend them on the global stage.

Still Have Questions About Buying Dollars with Rands?

Even when a process seems straightforward, it’s only natural to have a few questions pop up, especially when it involves your own money. Let's tackle some of the most common queries we hear from people just before they make their first ZAR to USD conversion.

Are These Platforms Even Legal and Regulated?

This is probably the most frequent question, and it's a good one to ask. Is it actually okay to use a digital service instead of your bank to exchange currency?

The answer is a resounding yes. Any financial technology company that offers these services in South Africa must be an authorised financial services provider, just like the big banks. They operate under the exact same stringent FICA and anti-money laundering regulations. That initial verification process isn't just a box-ticking exercise; it's a crucial step that ensures everything is secure and fully compliant with national financial standards.

What About Limits? How Much Can I Actually Exchange?

Another hot topic is transfer limits. "So, how much can I actually send over?" South Africa has clear exchange control regulations, which are set by the South African Reserve Bank (SARB). These rules apply to everyone, whether you walk into a bank branch or use a platform like Zaro.

For individuals, it breaks down into two main allowances:

- Single Discretionary Allowance (SDA): Every South African resident over 18 gets an allowance of R1 million per year to send offshore. This covers a whole host of things, from travel money to gifts for family abroad, and you don't need a tax clearance certificate for it.

- Foreign Investment Allowance (FIA): If you need to send more, you can tap into your FIA. This gives you an additional R10 million per year, but it's specifically for investment purposes and requires a Tax Compliance Status (TCS) PIN from SARS.

Modern platforms are designed to make navigating these allowances simple. They’ll usually guide you on which one fits your transaction, taking the guesswork out of the equation. For businesses, the limits are a bit different and are usually based on your documented needs, like paying an international supplier. Again, the platform will help you sort out the necessary paperwork.

The main thing to remember is that a digital platform doesn't let you bypass the rules—it just makes them a whole lot easier to follow. The system is built to keep your transactions well within the legal limits, saving you a massive administrative headache.

How Safe is My Money, Really?

Finally, let's talk security. Is your money as safe in a digital wallet as it is sitting in your traditional bank account? It's a perfectly valid concern.

Reputable platforms use top-tier, enterprise-grade security to protect you. Think advanced encryption and multi-factor authentication, all designed to keep anyone who isn't you out of your account.

Beyond that, your funds are typically held in segregated accounts at major partner banks. This is a critical detail. It means your money is kept completely separate from the company's own operating funds, which provides a powerful layer of protection. When you buy dollars with rands through a trusted service, you’re getting the best of both worlds: bank-level security fused with better technology and a far more transparent process.

Ready to see how a smarter, more transparent way of managing currency feels? With Zaro, you get the real exchange rate, crystal-clear fees, and a secure platform built for South Africans. It’s time to stop losing money to hidden markups and start handling your global payments with genuine confidence.

Learn more and open your account over at usezaro.com.