Sending money overseas from South Africa should be simple, but let's be honest—it rarely is. For too many businesses, it’s a minefield of hidden fees and frustratingly slow transfer times. The secret isn't just to find a cheaper bank; it's to sidestep the old system entirely. This is where modern platforms like Zaro come in, offering real exchange rates and faster payments that tackle the core problems eating into your bottom line.

Moving Beyond Traditional International Payments

If your South African company deals with anyone outside the country, you know that efficient cross-border payments are non-negotiable. They're a core part of staying competitive. Yet, many businesses are still stuck with legacy banking systems, and the pain points are all too familiar.

First, there are the surprise fees that sneakily drain your capital. I’ve seen traditional banks charge anywhere from R650 to R950 per international transfer just for the privilege of sending your money. And that’s before intermediary banks decide to take their slice of the pie. Then you have the exchange rates, which are often loaded with a hefty markup over the real market rate, directly impacting your profit on every single transaction.

The True Cost of Slow and Opaque Transfers

On top of the costs, slow processing times create a serious operational drag. When a payment takes three to five business days to actually arrive, it can hold up supplier shipments, mess with project timelines, and put a real strain on your relationships with international partners. This isn't just an annoyance; it creates genuine financial uncertainty.

And we're talking about a massive amount of money moving back and forth. In 2023 alone, South Africa recorded net current transfers from abroad at over -2.1 billion USD, a figure that highlights just how much capital is crossing our borders. You can dig into the specifics of these financial flows over at the World Bank.

The real challenge isn't just about sending the money. It's about doing it with predictability, transparency, and speed. Your business needs a system that gives you clarity, not more confusion.

A Modern Approach to Global Payments

This is exactly why platforms built for the way we do business today, like Zaro, are such a game-changer. They’re designed from the ground up to eliminate the very frustrations that make traditional international payments so painful. Forget about opaque fees and inflated rates; what you get is a clear, straightforward process.

For instance, the Zaro dashboard gives you a single command centre for all your cross-border transactions.

This kind of interface gives you an immediate, real-time view of your cash flow, letting you manage your funds without having to wrestle with a clunky old banking portal. In this guide, I'll walk you through exactly how to put a system like this to work for your business.

Preparing Your Business for Global Transactions

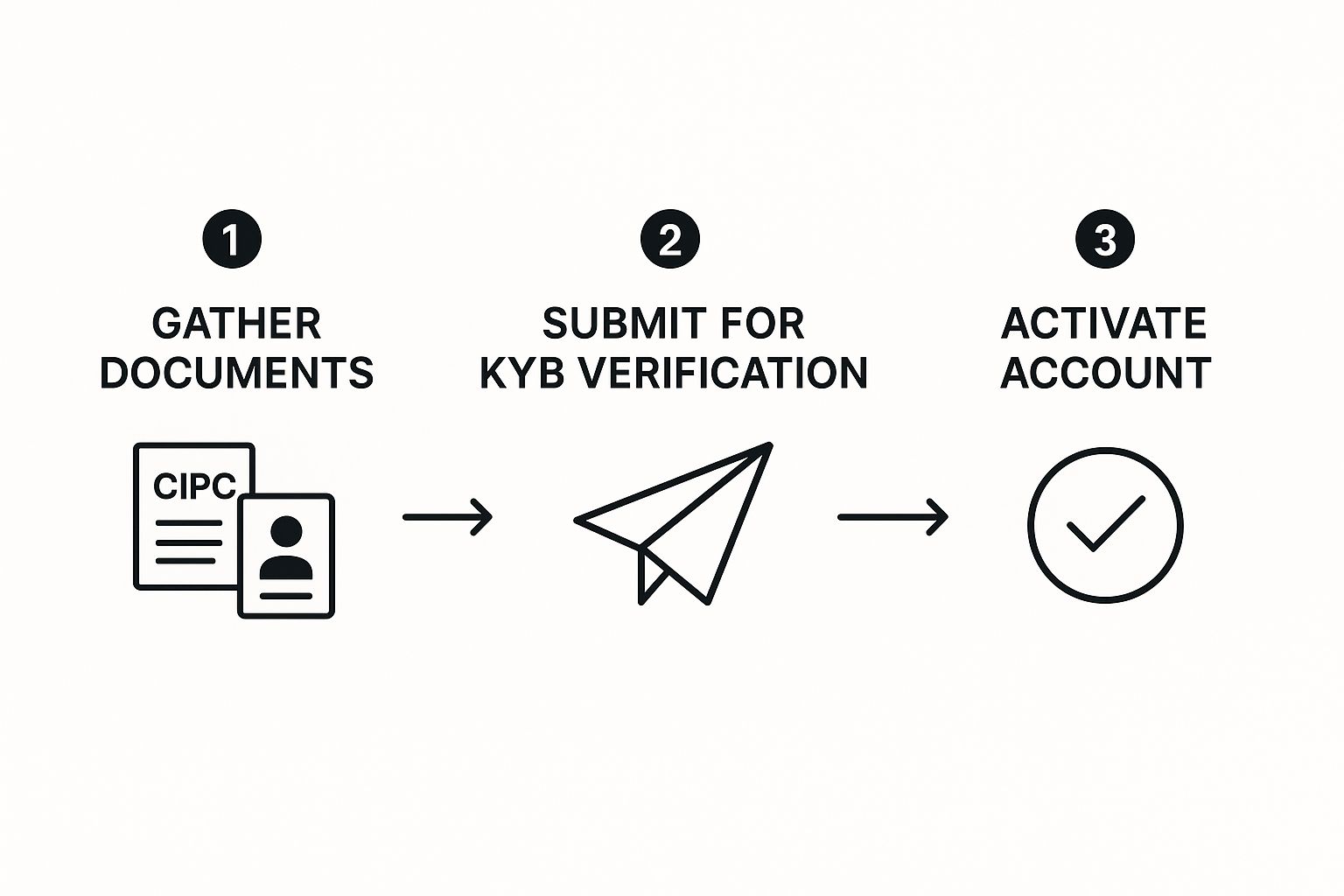

Before you can even think about sending money across borders, you need to get your house in order. This first part of the process is all about getting your business set up and verified, and it’s something you definitely don’t want to rush. Getting it right from the start is the key to making sure your future transactions are secure, compliant, and—most importantly—happen without a hitch.

For any South African business, this initial stage is built around Know Your Business (KYB) verification.

If you’ve ever had to FICA yourself, think of KYB as the business version of that. It's a non-negotiable check that confirms your company is legitimate. This process is essential for preventing fraud and meeting anti-money laundering regulations, and from experience, I can tell you that trying to cut corners here is the quickest way to get your account activation delayed.

Get Your Documents Ready Before You Start

My best piece of advice? Gather all your paperwork before you even click the "sign up" button. It makes everything so much smoother. While the specifics can differ slightly, if you’re running a South African PTY (Ltd), the list of required documents is pretty standard.

Here’s a checklist of what you should have scanned and ready to go:

- Company Registration Documents: Your official CIPC papers are a must. Think of your CoR 14.3 and any other incorporation documents.

- Proof of Business Address: A utility bill or bank statement showing your company’s physical address is perfect. Just make sure it’s less than three months old.

- Director and Shareholder Information: You’ll need certified ID copies for every director and any shareholder who owns 25% or more of the company.

- Tax Information: Have your company’s VAT number and any other SARS-related tax details handy.

Take a few minutes to digitise these and give them clear filenames. Trust me, "CoR_14.3_MyBusiness.pdf" is a lot easier to find and upload than "scan_001.jpg". It’s a small bit of admin that saves a lot of headaches.

Why All This Paperwork Matters

It can definitely feel like you’re just jumping through administrative hoops, but there’s a good reason for it. This KYB process is what allows platforms like Zaro to operate securely. It’s how they confirm you are who you say you are, which protects your business—and the entire financial system—from those looking to exploit it.

This level of diligence is what underpins the entire world of modern, fast, and secure international payments. For businesses expanding their footprint, a key part of this preparation involves setting up the right financial structures abroad, which might include things like opening a UAE company bank account if you're active in that market.

Pro Tip: Before you upload anything, check the expiry dates on all your documents. You'd be surprised how often an expired director's ID gets a verification submission kicked back, forcing you to start all over again.

Once you’ve submitted your documents, the platform’s compliance team takes over. They'll verify your details against official records. This is where things can get stuck. If the address on your utility bill doesn’t perfectly match the one registered with the CIPC, for example, it will almost certainly trigger a manual review and slow things down.

The simplest way to avoid this is to do a quick consistency check yourself before hitting ‘submit’. Make sure the company name, registration numbers, and addresses are identical across all your documents. It’s the single best thing you can do to sail through onboarding.

With your verification sorted, your account will be activated, and you’ll be all set to fund it and make your first international transfer.

How to Fund Your Account and Lock In Exchange Rates

Alright, so your KYB verification is done and dusted. Congratulations, your business is officially in the game! Now comes the important part: getting some funds into your account so you can actually start sending money across borders.

For South African businesses using Zaro, this is refreshingly simple. You can forget about the usual headaches that come with international wire instructions. Instead, you just top up your Zaro wallet with ZAR using a standard local Electronic Funds Transfer (EFT). It’s no different from paying a local supplier—a familiar process that settles quickly and skips the crazy fees that usually come with cross-border funding.

Getting through this verification process means your account is secure, compliant, and ready for whatever you need to throw at it.

Get Ahead of Currency Volatility

Once your ZAR balance is loaded, you've got a massive advantage: you’re in control of the exchange rate. This is where things get interesting. You're not just a passenger anymore; you're in the driver's seat of your international payments.

Most people don't realise that traditional banks bake their profits into poor exchange rates. With a platform like Zaro, you get access to the real mid-market rate—the one the banks use between themselves. This transparency is a game-changer. You see the true cost of your transfer, with no nasty surprises or hidden markups.

The rand's performance against currencies like the US dollar is a huge factor in what your international payments will actually cost. We’ve all seen how volatile it can be. For example, in mid-2024, the rand was trading around R17 to the dollar, but by the time of writing, it had slipped to R19. That kind of shift can make your US-based suppliers or software subscriptions a lot more expensive, almost overnight. You can find more insights on how currency fluctuations impact South African businesses on southafricanbusinessmatters.co.za.

Here’s a real-world look at the potential savings on a R100,000 transfer to the USA, showing how exchange rate markups and hidden fees add up.

Comparing Transfer Costs: Traditional Bank vs. Zaro

| Fee Component | Typical Bank Transfer | Zaro Transfer |

|---|---|---|

| Exchange Rate Markup | Banks often add a 2-4% markup | 0% (Uses real mid-market rate) |

| Hidden "Commission" | R2,000 - R4,000 | R0 |

| Swift/Admin Fees | R300 - R750 | R0 (on most major currencies) |

| Total Estimated Cost | R2,300 - R4,750+ | R0 (plus a small, transparent fee) |

As you can see, the hidden costs buried in a bank's inflated exchange rate are often where you lose the most money.

Lock In Your Rate and Protect Your Margins

Spotting a good exchange rate is one thing, but being able to act on it is what really protects your profit margins. This is where rate-locking tools become an absolute must-have for any business paying international invoices.

Let's say you have a $5,000 invoice due to a US software provider at the end of the month. You log in today and see the ZAR/USD rate is looking strong, but you're worried it will weaken by the time you have to pay. Instead of crossing your fingers and hoping for the best, you can lock in today's rate.

It’s incredibly straightforward:

- See the Live Rate: The real-time exchange rate is right there on your Zaro dashboard. No guesswork.

- Lock It In: With a couple of clicks, you secure that rate for your upcoming payment. The exact ZAR amount needed is set aside from your balance.

- Send with Certainty: When the invoice is due, you execute the transfer using the rate you already locked in, no matter what the live market is doing that day.

This isn't just a neat feature; it's a powerful financial strategy. By locking in a rate, you turn an unpredictable future expense into a known, fixed cost. It gives you total certainty over your international payables.

This level of control takes all the guesswork and risk out of the equation. It means the price you quoted a client or the budget you set for an overseas expense stays accurate, shielding your bottom line from the chaos of the foreign exchange market.

Making Your First International Payment with Confidence

With your Zaro account funded, it's time for the main event: sending that first payment. Honestly, this is where a lot of businesses feel a bit of a nail-biting moment, but the process is incredibly straightforward.

Let's walk through a common scenario for a South African business. Say you've got an invoice for €2,500 from a software supplier in Germany. It’s a standard operational cost, but with a traditional bank, you’d be bracing for vague fees and a poor exchange rate. With Zaro, you're in the driver's seat.

First, Add Your Beneficiary

Before you can send any money, you need to tell the system who you're paying. This means adding your German supplier as a new beneficiary. Think of it as adding a contact to your phone book—you only have to do it once for each international partner.

Head over to the 'Beneficiaries' section on your dashboard. You’ll be prompted to enter their details, and my best advice here is to be meticulous. Accuracy is everything.

For a supplier in Europe, you'll need two key pieces of information:

- Their IBAN (International Bank Account Number)

- The bank’s BIC/SWIFT code

Double-check every single character before you hit save. I can't stress this enough—a single typo is the number one culprit behind failed or delayed transfers. Taking an extra 60 seconds here can save you days of headaches later. Once saved, that supplier is locked in, making future payments a simple two-click affair.

Here's a pro-tip from my own experience: The first time you pay a new major supplier, send a small test payment, maybe €10. It’s a tiny investment to confirm all the banking details are spot-on. This gives both you and your partner complete confidence before you transfer a much larger sum.

Executing the Transfer with Total Clarity

Once your beneficiary is set up, you're ready to make the payment.

You'll select your supplier from the list, pop in the payment amount (€2,500 in our example), and choose which of your currency wallets you want to pay from. The platform instantly shows you the live, real-time exchange rate and the final ZAR amount that will be debited. All fees are laid out, plain and simple.

This is the moment of truth. You see exactly what you’re paying, with zero hidden costs. The interface gives you one last summary to review everything before you commit.

Here’s a look at what that final confirmation screen looks like—it’s all about giving you a clear breakdown before you click send.

This screenshot shows that final step, giving you complete transparency over the transaction before the money moves.

Once you hit confirm, the payment is officially on its way. Forget that old feeling of funds disappearing into a black hole for days. Zaro gives you real-time tracking right from your dashboard. You can watch its progress from processing to the moment it lands in your supplier’s account.

Most transfers to major corridors like Europe or the US are completed within 1-2 business days, a huge leap from the 3-5 day waiting game with many banks. When the funds arrive, you get a final confirmation. Loop closed, peace of mind restored.

Smarter Ways to Manage Your International Payments

Sending money across borders is one thing, but truly mastering it requires a shift in mindset. Instead of just reacting to invoices as they land, your business can gain a real competitive edge by building a financial strategy around your global payments. It’s about turning a necessary chore into a powerful tool for managing your cash flow.

Many South African businesses get stuck in a reactive cycle: an international invoice comes in, and they immediately convert ZAR to pay it. The problem? You're completely at the mercy of that day's exchange rate, which is a gamble that can quietly eat away at your profits over time. There's a much smarter way to operate.

Timing Your Transfers and Using Multi-Currency Wallets

This is where a multi-currency wallet becomes your most valuable asset. Imagine having the ability to hold different currencies—like USD, EUR, or GBP—without the headache and red tape of opening foreign bank accounts. That's exactly what it does.

Let's say a client in the US pays your invoice. Instead of that money being automatically converted to Rand, it can sit safely in your USD wallet.

This simple change gives you incredible flexibility and control.

- Hold Funds Strategically: You’re no longer forced to convert your dollars to rand on a day when the rate is poor. You can hold onto the USD and wait for a more favourable exchange rate, protecting your bottom line.

- Pay in Local Currency: Got a US-based software subscription or supplier to pay? You can pay them directly from your USD wallet. This move completely sidesteps the need for a currency conversion and its associated fees. Brilliant.

This approach weaves your international payments directly into your financial planning. While we're focused on business transactions here, it's interesting to see how this compares to personal remittances. In 2020, remittance inflows only made up 0.24% of South Africa's GDP, but they're still a vital source of income for countless families. You can dig into more of this data on South Africa's financial inflows on tradingeconomics.com.

Keeping SARS Happy with Clean Records

For any South African business sending money internationally, solid documentation isn't just a "nice-to-have"—it's a must. Staying on the right side of SARS means keeping meticulous records, and that’s a non-negotiable part of the game.

Trying to keep track of every payment with a patchwork of spreadsheets and saved PDFs is a recipe for disaster. It’s tedious, prone to human error, and a massive time-sink.

This is why modern payment platforms are such a game-changer. They automate the entire record-keeping process for you, generating clean, clear statements and transaction histories for every single payment.

When tax season rolls around, or if you're ever audited, having a complete, easily accessible history of every cross-border transaction is invaluable. It transforms a painful administrative burden into a simple, automated part of your workflow. That means less time drowning in paperwork and more time focused on what actually matters: growing your business.

Common Questions About Sending Money Internationally

When you're running a South African business that operates globally, sending money across borders can bring up some serious questions. Let's face it, you need straight answers to make smart decisions with your company's cash. We've tackled the most common queries we hear from businesses just like yours.

First up, speed. Everyone wants to know: "How long will it really take?" We've all been stung by traditional bank wires that crawl along, sometimes taking 3 to 5 business days. Thankfully, that's not the standard anymore. With modern platforms, transfers to places like the UK, Europe, or the US can often land within 1-2 business days. Some routes are even faster, hitting the recipient's account the very same day.

Paying your team abroad is another big one. If you have international employees or freelancers, how do you handle their payroll without headaches? It's actually one of the best use cases for a service like Zaro. You can pay people directly in their local currency, right into their bank accounts. This sidesteps the terrible exchange rates and hidden fees that often eat into their earnings.

Understanding the Legal Requirements

For any South African business, compliance isn't just a buzzword—it's essential. So, what are the legal hoops you need to jump through? Every single international payment you make falls under the watchful eye of the South African Reserve Bank (SARB) and FICA regulations.

This boils down to a few key things:

- You need a valid reason for the payment, like an invoice for imported goods or a service contract.

- Your business must complete a Know Your Business (KYB) verification to confirm its identity.

- You have to maintain meticulous records of all your international transactions for reporting.

A good payment platform will walk you through these steps, making sure every transfer is above board. It’s a similar world for your team members living abroad; when they sort out things like international health insurance for expats, they're also dealing with cross-border payments, which just shows how common this need is.

The point of a modern payment system isn't to find loopholes in the rules; it's to make following them incredibly simple. When compliance checks are built right into the process, it takes a massive administrative weight off your team's shoulders.

At the end of the day, sending money overseas should be a tool for growth, not a source of frustration. Once you get a handle on the timelines, use cases, and legal must-dos, you can manage your global finances with confidence and keep your focus where it belongs: on building your business.

Ready to stop overpaying on international transfers? With Zaro, you get access to real exchange rates and a powerful platform built for South African businesses. Start sending money smarter today.