Sending money out of South Africa can feel like a mission. It often seems bogged down by confusing rules and hidden fees. But here's the thing—it doesn't have to be that complicated.

Whether you're supporting family back home, paying for your child's overseas tuition, or making an international investment, the right service can make the process simple and surprisingly affordable. Modern platforms like Zaro are a world away from the old-school banks, focusing on getting your money where it needs to go quickly, safely, and without breaking the bank.

Getting to Grips with International Money Transfers

Sending money across borders isn't just another transaction; it’s a critical part of the economy for countless people and entire countries. For South Africans, in particular, being able to move cash abroad is a lifeline for both personal and business needs, contributing to a steady stream of funds leaving the country.

This outward flow is more significant than you might think. In 2023, South Africa recorded a net outflow of roughly -$2.16 billion in current transfers. That number tells a clear story: far more money was sent out than came in, cementing the country's role as a major source of remittances for the region and globally.

Why Are We Sending Money Abroad?

The reasons people send money overseas are as varied as the people themselves, but they usually boil down to a few core needs:

- Family Support: This is a big one. Many of us send money to help relatives living in other countries.

- Education: It's common for South Africans to pay for university or school fees for family members studying abroad.

- International Investments: From buying property to snapping up shares, many are looking for opportunities in foreign markets.

- Business Payments: If you run a business, you know the drill—paying overseas suppliers or international contractors is a regular necessity.

Making Sense of the Rules

Before you even think about hitting 'send', you need to know the rules. The South African Reserve Bank (SARB) has a tight grip on capital flows, and you have to play by their book. Sticking to the guidelines is the only way to avoid frustrating delays or, worse, legal trouble.

I always tell people the same thing: understanding the regulations is the secret to a stress-free transfer. Know your annual allowances and have the right documents ready before you start.

It's also a good idea to familiarise yourself with the broader regulatory landscape. This includes understanding relevant sanctions enforcement policies, as they can have a massive impact on your ability to send money internationally. Getting a handle on these rules ensures your funds don't get stuck in limbo.

Honestly, choosing a service that guides you through this maze is half the battle won. It just makes the whole process so much easier.

Getting Your Documents and Details Ready

Before you can send cash overseas, a little bit of homework goes a long way. Think of it as a pre-flight check for your money to ensure everything goes smoothly and stays above board. Any legitimate financial service in South Africa, including digital platforms like Zaro, is required by law to verify who you are.

This isn't just red tape; it's part of complying with the Financial Intelligence Centre Act (FICA), which is crucial for preventing financial crime. So, you’ll need to have clear copies of a few key documents handy.

Your Personal and Business Information

The required paperwork depends on whether you're sending money personally or for your business. For personal transfers, it's pretty straightforward. Business transactions just require a few extra items.

- A valid South African ID: Your green bar-coded ID book or a smart ID card will do the trick.

- Proof of residential address: A recent utility bill or a bank statement (no older than three months) is perfect, as long as it clearly shows your name and physical address.

- Business Registration Documents: If the transfer is on behalf of a company, you’ll need your CIPC registration documents and similar official papers.

Essential Recipient Details

I can't stress this enough: accuracy here is everything. A single typo in an account number or a name can cause massive delays, or worse, your funds could be sent back—often with a fee deducted.

Before you even think about hitting 'send', double-check that you have this information from your recipient:

- Full legal name: It must match their bank account name exactly.

- Physical address: Their complete residential or business address.

- Bank name and branch: The specific bank and branch where their account is held.

- Account number: For many regions, especially Europe, this will be an IBAN (International Bank Account Number).

- SWIFT/BIC code: This is a unique code that acts like a global postcode for banks, directing your money to the right institution.

My best advice? Always ask the recipient to email or message you their banking details. This way, you can copy and paste everything directly, which practically eliminates the risk of a costly manual error.

Understanding South African Exchange Control

South Africa has some specific rules about how much money individuals can send overseas. These regulations are managed by the South African Reserve Bank (SARB), and it’s important to know the limits before you start.

The main allowance for individuals is the Single Discretionary Allowance (SDA). This lets every South African resident over 18 send up to R1 million abroad per calendar year. You can use it for almost any legal purpose, and you don’t need to get a Tax Compliance Status (TCS) PIN from SARS.

If you need to send more than R1 million, you can tap into your Foreign Investment Allowance (FIA). This gives you an additional R10 million per calendar year. However, using this allowance means you must first get a TCS PIN from SARS to prove your tax affairs are in order.

The screenshot below, taken directly from the SARS website, lays out these allowances clearly.

As you can see, the official guidance confirms the different limits for discretionary and investment purposes. Honestly, getting all your ducks in a row before you start is the single best thing you can do to make the whole process completely hassle-free.

Your First International Transfer: A Practical Walkthrough

Enough with the theory. Let's get down to brass tacks and walk through exactly how you’d send money abroad with a modern platform like Zaro.

Imagine this real-world scenario: you need to send R20,000 to a family member studying in the United Kingdom. This isn't just a dry list of instructions; it's a step-by-step guide to show you how straightforward the whole process can be.

The first hurdle is always setting up and verifying your account. Digital platforms have made this worlds faster than the old-school banks, but they’re just as secure. You'll need to upload your FICA documents (your ID and a recent proof of address). Verification is usually pretty quick, and once that’s done, you’re clear to add your first recipient.

Getting Your Recipient and Transfer Details Right

This is the part where you want to be meticulous. In the app, you’ll find a section like "Add Recipient" or "Manage Beneficiaries." Here, you’ll carefully enter their full name, physical address, and their UK bank details—specifically, their account number and sort code.

My advice? Always double-check these details. Get them to send you a screenshot or copy-paste the information directly from their banking app. A single typo can cause major delays.

Once your recipient is saved, you’re ready to set up the R20,000 transfer. As you type in the amount in ZAR, the platform will instantly show you the equivalent in British Pounds (GBP) using the live exchange rate. This transparency is a game-changer; you know precisely what they'll receive before you hit 'send'.

Here’s a pro tip: many modern platforms let you lock in an exchange rate. If you see a rate you’re happy with, you can secure it for a short period. This is brilliant because it protects you from any sudden market dips while you get your funds sorted.

After you've confirmed all the details, you'll fund the transfer. This usually just means making a standard Electronic Funds Transfer (EFT) from your South African bank account to the platform's local FNB or Nedbank account. They'll give you a unique reference number to use, which is how they tie your deposit to your transfer. It’s a simple, low-cost way to get the money into their system.

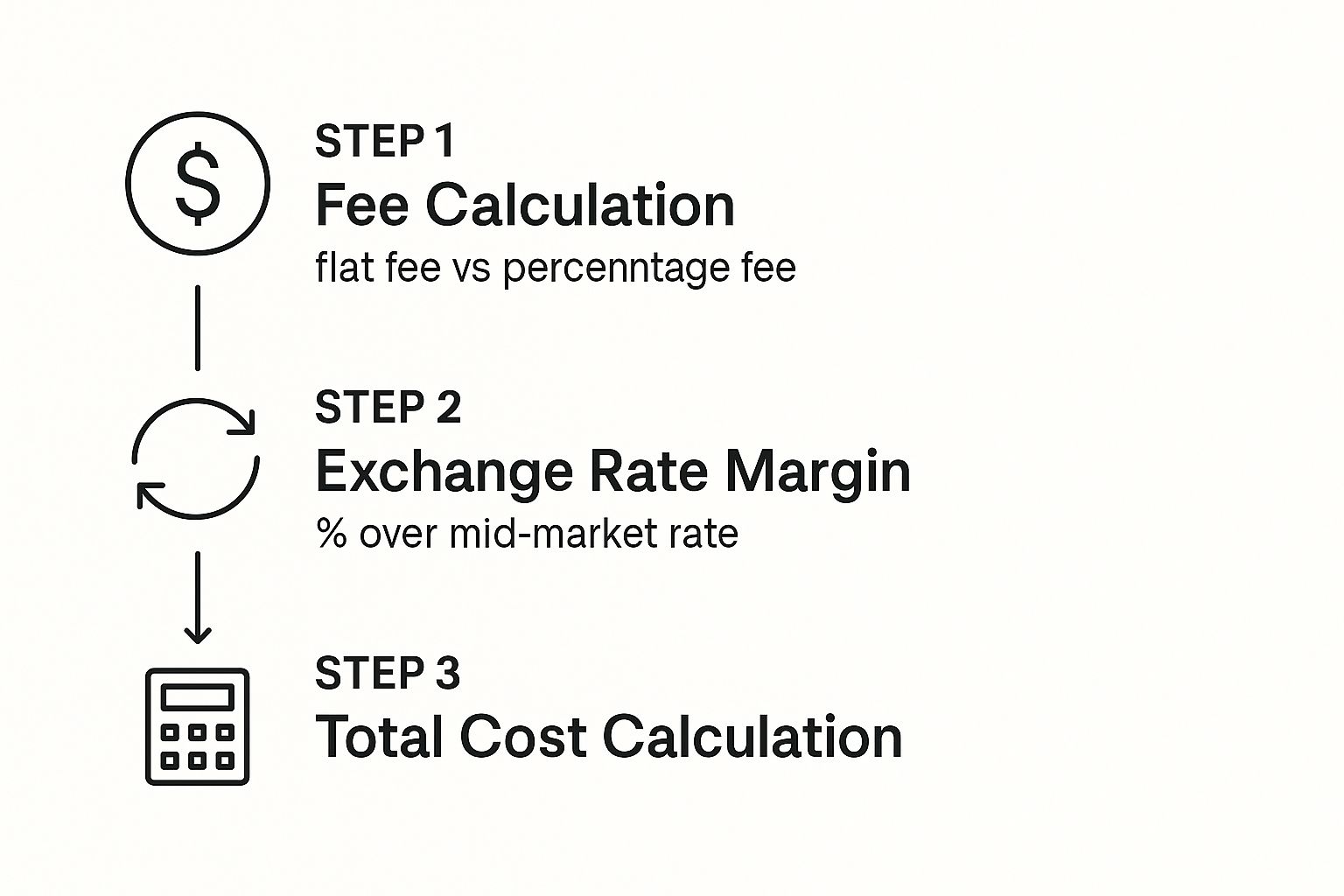

This infographic breaks down what really goes into the total cost of sending money abroad.

Getting a handle on these two parts—the upfront fee and the exchange rate margin—is the key to understanding the true cost and picking the smartest option.

From Your Account to Theirs: Tracking and Confirmation

Once Zaro receives your EFT, their team takes over for the international leg of the journey. This is where modern services really shine. Instead of waiting and wondering, you get real-time tracking. You’ll receive email or app notifications at every critical stage:

- Funds Received: A confirmation that your ZAR has landed safely in their account.

- Payment Processing: The alert that your money is being converted and dispatched across the SWIFT network.

- Payment Delivered: The final, welcome notification that the GBP has been deposited into your family member's UK bank account.

This level of visibility takes all the stress and guesswork out of the equation. As you look into different services, it's helpful to see how new financial technologies are solving these age-old problems. If you're curious about where things are headed, you might find it interesting to read about the potential of blockchain technology for efficient international payments. Ultimately, the goal is always to reduce friction and cut costs—exactly what you should be looking for in a provider.

Uncovering the True Cost of Your Transfer

When you need to send money overseas, it’s easy to get fixated on the advertised transfer fee. But that’s a classic mistake. The real sting often comes from a place most people don’t even look: the exchange rate.

This is where many traditional services make their real money. You see a rate on Google or a news site—that’s the mid-market rate. Think of it as the 'real' exchange rate that banks use when they trade massive amounts of currency with each other. It’s the fairest rate you can get.

But it’s almost never the rate you’re offered. Instead, banks and older transfer services quietly add a markup, or a "spread," on top of that rate. They’re essentially selling you the foreign currency for more than it’s worth. A markup of 2-3% might sound trivial, but on a significant transfer, that hidden cost can easily climb into hundreds, or even thousands, of rands.

Decoding the Fees

Once you’re wise to the exchange rate game, the next thing to watch is the upfront fee. These tend to fall into two camps, and knowing which is which helps you pick the right service for your needs.

- Flat Fees: You pay a single, fixed charge no matter how much you send. This model usually works out better for larger transfers because the fee becomes a tiny slice of the overall amount.

- Percentage-Based Fees: The service takes a cut of the total amount you’re sending. This can be great for small, quick transfers but gets expensive fast as the transfer amount grows.

High costs are a serious problem, particularly for transfers within the continent. Sending money to African countries remains stubbornly expensive, with average fees hovering around 5% in 2023—way above the UN’s target of 3%. These high costs from banks and mobile money providers are a major reason why many people still turn to informal, and often riskier, methods. You can discover more about the impact of remittance costs in Africa to get a deeper understanding of this challenge.

The true cost of your transfer is always the upfront fee plus the hidden exchange rate markup. Always calculate the final receiving amount to see who offers the best value.

A Real-World Cost Comparison

Let’s put this into perspective. Say you need to pay a UK-based supplier R25,000. The difference between using your old-school bank and a modern digital service like Zaro is staggering.

Here’s a simple breakdown that shows where your money actually goes.

Cost Comparison: Bank vs. Digital Service (Sending R25,000 to the UK)

| Feature | Traditional SA Bank | Digital Transfer Service (Zaro) | What This Means for You |

|---|---|---|---|

| Exchange Rate | Mid-market rate + 2.5% markup | Real mid-market rate (zero markup) | You lose R625 to the bank's hidden fee before you even start. |

| Upfront Fee | R400 (flat SWIFT fee) | R0 (no transfer fees) | An immediate and clear saving on the transaction cost. |

| Total Cost | R1,025 (R400 fee + R625 markup) | R0 | You save over a thousand rand on a single transfer. |

| Recipient Gets | Significantly less due to fees | The full amount converted at the best rate | Your recipient gets more money, which is always good for business relationships. |

The numbers don't lie. By opting for a service that gives you the real exchange rate and ditches the unnecessary fees, you ensure more of your money arrives where it’s needed. This kind of transparency isn’t just a nice-to-have; it’s essential for anyone who wants to move money across borders efficiently and without getting ripped off.

Best Practices for Safe and Efficient Transfers

Getting your transfer sent is one thing, but making sure it's done safely and cost-effectively is where the real expertise comes in. After you’ve settled on a provider like Zaro, a few good habits can make all the difference, helping you sidestep common headaches and protect your money.

The single most important thing you can do? Double-check every single detail before you hit that 'send' button. It sounds simple, but you'd be surprised how often a small typo in a name or account number leads to major delays. Sometimes the money even gets bounced back, and you could be hit with a recall fee for the trouble.

My go-to tip: always ask the recipient to send their details in writing. Then, copy and paste everything directly to avoid any manual entry errors. It takes a few extra seconds but can save you days of stress.

Lock Down Your Account and Information

When you’re sending cash abroad, you need to treat your transfer account with the same seriousness as your main bank account. This all starts with the basics: create a strong, unique password that isn’t a carbon copy of the one you use for your streaming service.

Better yet, always switch on two-factor authentication (2FA) if it’s available. This is a game-changer for security. It means that even if someone manages to guess your password, they can't get into your account without a second piece of proof, like a one-time code sent to your phone.

Think of these small steps as your first line of defence. They’re simple, effective, and crucial for keeping your funds safe from fraud.

"A good rule of thumb: never share your login details with anyone. Be suspicious of any unsolicited emails or messages asking for personal info—a legitimate financial service will never ask for your password over email."

Timing Your Transfer and Staying Vigilant

Believe it or not, timing can have a real impact on how much money lands in your recipient's account. Exchange rates are constantly on the move, shifting with the pulse of the global markets. You can't predict the future, but you can be smart about it.

If your transfer isn’t urgent, it pays to watch the exchange rate for a day or two. Many platforms even let you set up rate alerts, which will ping you when the rate hits a number you’re happy with. Locking in a rate that’s just a few cents better might not seem like much, but it can add up to a significant saving on larger amounts.

Finally, and this is non-negotiable, always use a regulated provider. Here in South Africa, that means picking a service that is an authorised dealer or works with one, so you know they are compliant with SARB regulations. An unregulated provider might dangle a cheaper fee, but the risk of losing your money entirely, with no one to turn to, just isn’t worth it. Your peace of mind is priceless.

Common Questions About Sending Money Abroad

Even with a solid plan, a few questions always seem to pop up when it's time to send money overseas. I get it. It's a process with a lot of moving parts, and you want clear, straightforward answers before you commit.

Let’s run through some of the most common queries I hear from South Africans who are getting ready to make an international transfer.

First up, the big one: timing. Everyone wants to know, "How long will my transfer actually take?" The honest answer is, it really depends on who you use. If you go the traditional route with a bank, you could be waiting anywhere from 3 to 5 business days. Sometimes it’s even longer if there are intermediary banks slowing things down.

Modern digital platforms like Zaro, on the other hand, have changed the game. They can often get the funds there in just 1 to 2 business days, and some currency routes are even quicker. The final speed always depends on a few factors, like the destination country, how fast the recipient’s bank processes incoming payments, and even the time of day you hit 'send'.

What Are the Transfer Limits?

Another question that comes up constantly is about transfer limits. This is a big deal because of South Africa’s exchange control regulations, and it’s something you absolutely need to get right.

To recap, you have two main allowances you can use:

- Single Discretionary Allowance (SDA): This is your go-to for smaller amounts. You can send up to R1 million abroad per calendar year without needing to get a Tax Compliance Status (TCS) PIN from SARS.

- Foreign Investment Allowance (FIA): If you need to send more than R1 million, you can tap into your FIA. This gives you an additional R10 million per year, but for this, you must have a valid TCS PIN from SARS.

Remember, these limits reset every calendar year. I always advise people to keep a simple record of what they've sent. It's the easiest way to make sure you stay well within the legal framework.

A key thing to remember is that these allowances are per person, per calendar year. So, for example, a married couple actually has a combined discretionary allowance of R2 million annually.

This structure gives most people more than enough flexibility for everything from personal transfers to overseas investments.

Can I Send Money to Any Country?

For the most part, yes, you can transfer money to almost any country. There are, however, a few exceptions. South African regulations and international sanctions mean you can’t send funds to certain high-risk or sanctioned nations.

Any reputable transfer service keeps an up-to-date list of these restricted destinations to stay compliant. If you have any doubt about a specific country, just ask your provider before you start the process. A quick check upfront can save you from a transfer being blocked or delayed down the line.

Of course, money flows both ways. While many South Africans are sending funds out, we also see remittances coming into the country. Back in 2020, these inflows were about 0.24% of our GDP. That might not sound like a huge number, but for countless families, especially in rural areas, that money is a lifeline. You can actually learn more about South Africa's remittance data to see the bigger picture. Getting these details right just makes sure your money gets where it needs to go, smoothly and without fuss.

Ready to make your international payments simpler and more cost-effective? With Zaro, you get the real exchange rate with zero markup and no hidden fees. Get started with Zaro today and see how much you can save.